Tariffs went into effect at midnight on Thursday. The evidence is building that tariffs could be inflationary for US consumers over the second half of this year. If tariffs do become inflationary, we could see a potential reduction in consumer spending, or at least their purchasing power, which does little to prop up manufacturing. However, it still remains to be seen if there could be a case built to say that tariffs alone will inspire enough domestic manufacturing of goods over time to increase domestic production. Given all the “remains to be seen” surrounding tariffs, the FED is in no rush to reduce interest rates and decided to hold again, however it is worth noting that two members dissented from the majority with a vote to cut at the last meeting.

Let’s dive a little deeper into these topics.

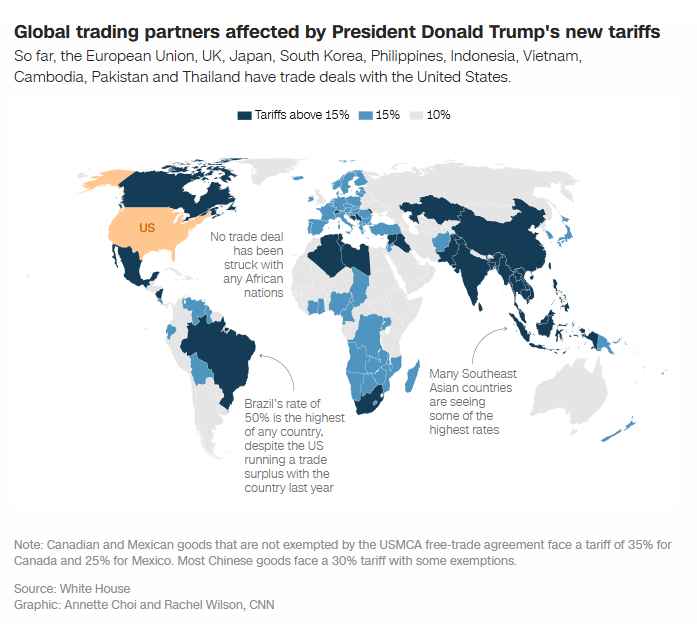

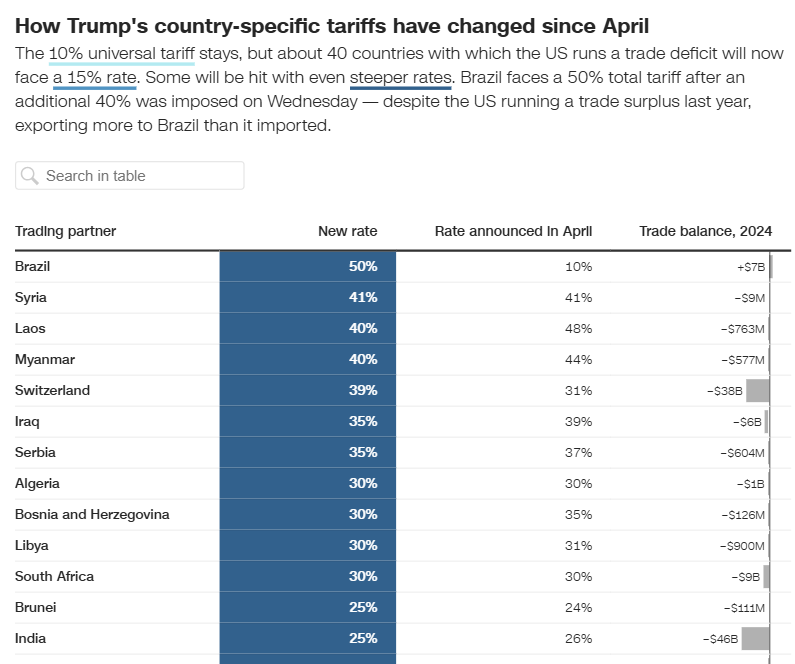

The tariffs that went into effect on August 7th were announced on April 2nd, but some were also more recent announcements and escalations or retaliatory tariffs. Some of the US’s trading partners secured reductions through negotiations and deals, including the UK, Thailand, Cambodia, Vietnam, Indonesia, the Philippines, Japan, South Korea, Pakistan and the EU.

China still faces a 30% rate, but negotiations are said to be ongoing before its separate August 12th deadline for higher rates. On Wednesday Trump doubled tariffs on India to 50% (set to take effect on August 27th) from the planned 25% due to India’s continued purchase of Russian crude oil. He has also threatened China with similar measures for their purchase of Russian oil. However, China made a statement saying their purchasing of Russian oil is legal and part of their economic activity. Trump is attempting to use secondary sanctions to apply pressure ultimately on Russia to end the Russian/Ukrainian War. It could work, or it could backfire, and push Russia, India and China even closer to each other and against the US.

But, as far as tariffs are concerned, it’s important to note that they are being used as a geopolitical pressure tool, not just a US tax source, which makes them even more volatile or unpredictable. Also on Wednesday, Trump warned that the US would impose a tariff of about 100% on semiconductor chips imported from countries not producing in America or planning to do so. It remains to be seen if that will materialize but so far many threats have become reality.

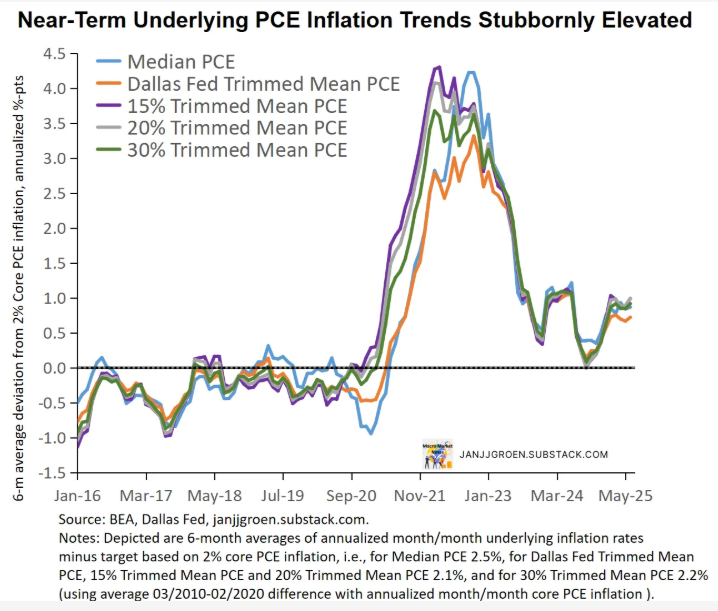

Keeping an eye on inflation measures going forward will be critical. The problem is that inflation has not yet met the desired 2% target, and it has not really showed signs of getting there in the last couple of years. Matthew Klein wrote,

“The bigger worry is that there has been little to no progress on inflation over the past 18-24 months, and that this was true even before tariffs started showing up in the data. While the direct impact of tariffs is limited by the fact that imported goods are only a small part of the total U.S. consumption basket, the indirect effects could be larger and longer-lasting as shell-shocked households and businesses are forced to deal with yet another set of arbitrary price spikes so soon after the pandemic and the Russian invasion of Ukraine.”

At the end of July we got the June PCE numbers which remain elevated in a 2.7%-3% core PCE inflation range on a six-month basis. Still above pace for a 2% inflation target. Supporting this would be the still steady consumer spending, although some signs of consumer caution are starting to show, and still increasing incomes and wage growth.

Jan Groen visualized the stubborn PCE measures here:

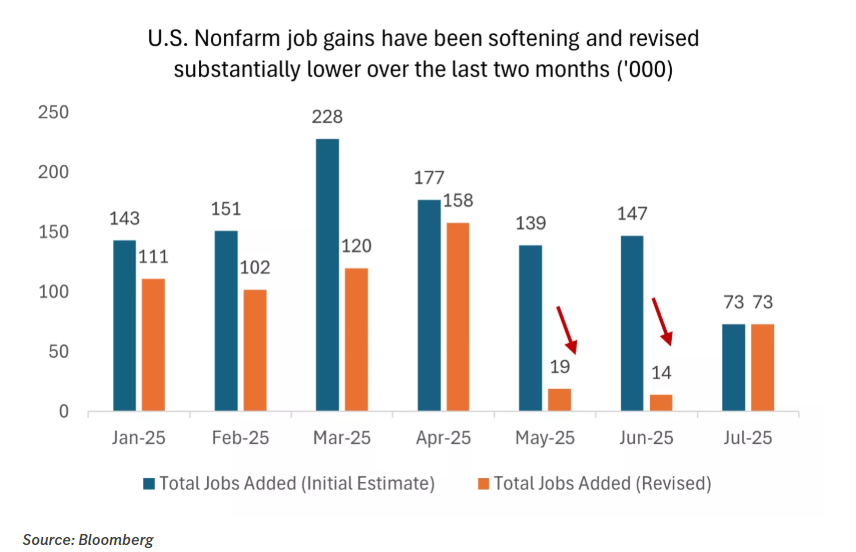

With inflation still higher than target, and wage growth still showing up, it’s important to understand the most recent jobs data. The FED has two jobs: control inflation, and keep a strong labor market. Inflation is lower than it was, but I’m not sure they would call it “controlled” right now, or at least it runs the risk of getting out of control again soon should they cut.

The latest jobs data, the noise around it, and the varying opinions of economists that I respect, gave me a bit of a headache as I tried to understand what exactly is going on and what it might mean for our future direction.

July’s jobs report showed just 73,000 new positions added, falling short of the 104,000 economists had expected. Adding to the disappointment, figures from the previous two months were revised down by roughly 260,000 jobs. With those adjustments, job growth over the past three months now averages 35,000 per month, a steep drop from the 127,000 monthly pace seen in the prior quarter. The unemployment rate moved from 4.1% to 4.2% as well. And as I mentioned previously in this newsletter, wage growth was strong at 3.9%, which outpaces the current 2.7-3% inflation rate, providing some context to the sustained consumer spendings and the still present consumer savings.

What does this mean?

Here are my thoughts on all of this. Revisions to monthly jobs data are routine, as the Bureau of Labor Statistics updates its initial estimates with more complete information, such as Unemployment Insurance records. However, the sharp downward adjustment of roughly 260,000 jobs over the past two months stands out as unusually large for consecutive months. While sizable revisions (sometimes in the hundreds of thousands) do occur, they are more commonly spread over longer periods or made during annual benchmark updates, rather than in back-to-back monthly reports. This makes July’s figures very notable, as consecutive months with such steep downward changes are rare in the historical record.

The revisions came after the FED’s decision to hold off on rate cuts, with Powell’s comments mentioning the “strong labor market”. So, the issue would be that these very significant revisions, because they were too late, could have impacted the FED’s latest decision. However, economists now expect that the updated view of the labor market will factor into the FEDs future decisions and might sway more members towards the view point of the two governors who dissented in the most recent vote.

“In our view, the sizable downshift in the jobs data indicates that the U.S. economy may be entering a softer growth patch. A softer labor market, combined with higher tariff rates, may put some pressure on the consumer and household consumption. However, we also believe that the Federal Reserve is now more likely to cut interest rates, as reflected by markets as well. While growth may slow in the coming quarters, we do not see a recession on the horizon, and as we head toward 2026, we could see a rebound as interest rates move lower and as some marginal fiscal stimulus from the tax bill kicks in.”

However, Q2 labor productivity data is out now as well, and we can see that productivity improved in Q2, employee wages increased in Q2, and hiring did indeed slow throughout Q2. So, while fewer jobs are being added, productivity gains were noted, and currently employed persons found themselves with marginally increasing wages, enough to continue to outpace inflation. Productivity gains, and reduced hiring also helped corporations reduce their exposure to the growing wages impacting their margins.

I wrote back in December or so that I believed that the loosening of restrictions/regulations by the current administration for AI and automation could have been in preparation to boost labor productivity in the US at a time where they seem determined to bring back some of America's manufacturing. Manufacturing left America because we were not as efficient and productive as other nations. Gad Levanon was my most recent guest on the Meet Me For Coffee Podcast last week, and he spoke highly of AI and the contributions it is making to many different industries' productivity. He anticipates it will only improve over the next year yes, but also for years to come. I've heard some optimists take the stance that the current administration has no appetite for a recession, but that instead they seem to be attempting to thread a fine needle that could, at some point in 2026, end up being worth the pain of the uncertainty in 2025. That said, I think almost any type of real rebound from all of this will be coming in 2026 and no sooner.

I was double checking source links before publishing today and realized Edward Jones and released their most updated outlook yesterday, and took a strong optimistic stance in my opinion. I found it interesting:

Nonfarm business sector productivity increased at a 2.4% annualized pace in the second quarter, beating estimates pointing to a 2.2% rise2. Despite a softer labor market, hourly compensation grew a healthy 4.2% year-over-year, comfortably above inflation of about 2.7%2. This means consumers, on average, are receiving positive real wage gains, which should provide disposable income to help support consumer spending and the economy, in our view. Productivity gains partially offset solid wage gains to keep unit labor costs, which adjust hourly wages for higher output, contained at 1.6% annualized2. We believe modest increases in unit labor costs, if sustained, should help counteract the impacts of tariffs on inflation.

So consumer spending has been holding up, inflationary impacts of tariffs are starting to be heard but not yet seen/felt in the spending. So what about manufacturing? Will tariffs hinder or spur manufacturing activity?

July’s PMI data showed overall PMI contracting to 48 vs. a 48 in June, and New Orders were up slightly to slow the pace of contraction. Notably, employment is contracting still, and July showed a faster pace. Reading through comments and survey results it would appear that manufacturers are taking a very cautious approach to hiring still (which also makes sense with strong wage reports), and making cautious business decisions around inventory and purchasing. Overall manufacturing activity is still fairly flat.

One of the intended purposes, at least the administration has said, of tariffs is to bring manufacturing back to the US. As most of us know, reshoring takes time. We are still seeing increases in trade with Mexico that was a result of the 2020 pandemic, and it’s 2025. Still, there are some chances that certain manufacturers speed up their US manufacturing faster than would be typical in order to avoid tariffs, like in the case of Apple.

Apple CEO Tim Cook met with President Trump at the White House on Wednesday to unveil a major new investment in U.S. manufacturing, an additional $100 billion over the next four years. This boosts Apple’s total domestic commitment to $600 billion. Just hours earlier, Trump warned of potential 100% tariffs on chips and semiconductors but assured that companies committed to building in the U.S. would be exempt. Apple’s latest plans include a smart glass production line in Kentucky, a new server manufacturing plant in Houston set to open by 2026, and a manufacturing academy in Detroit launching August 19. The company projects it will produce over 19 billion chips in U.S. facilities this year, including supply from TSMC’s new plant in Arizona.

While $100 billion of this investment is new, the rest has already been in progress and notice they say in the next four years. Nothing can move overnight, or in a president’s first year.

For freight market health, we need to see some strong growth in domestic manufacturing, and we may need another couple of quarters to see that begin. Consumer spending has remained already high, so for freight market health purposes what we cannot afford would be additional pullbacks of demand.

Meanwhile, the trucking market is facing increased competition by rail as rail providers are seeking to innovate their services to be more competitive. I found this new service announcement by Union Pacific particularly interesting. California based carriers or long haul expedited carriers have been facing down volatile demand with import volume irregularities in CA this year, and now they may face increased competition by the rail.

OMAHA, Neb.--(BUSINESS WIRE)--Aug. 7, 2025-- Union Pacific Railroad will launch a new, truck-competitive domestic intermodal service connecting Southern California’s Inland Empire to the heart of Chicago, significantly boosting intermodal capacity. Beginning Sept. 3, this innovative service enhances the seamless connection from the Los Angeles Basin's most active warehouse district through Union Pacific’s Inland Empire Intermodal Terminal (IEIT) directly to Chicago's Global 2 Intermodal Terminal. Customers will experience up to 20% faster intermodal service compared to current industry offerings between these key locations, with three days' transit. The service will start at five days a week with the ability to increase with growth. “As we continue expanding IEIT, this service will deliver consistent, reliable and truck-competitive transportation, challenging the norms of over-the-road shipping and competing head-to-head with team driver truck services,” said Kenny Rocker, executive vice president-Marketing and Sales, Union Pacific Railroad. This new offering is part of Union Pacific’s Z train network, providing the fastest delivery of time-sensitive freight. Visit UP.com for intermodal schedules.

A huge thank you to BiggerPicture for sponsoring this month's newsletter! BiggerPicture is focused on helping shippers, brokers, and carriers maximize their operational productivity, by reducing the time spent scheduling appointments by an average of 80%. Achieve full ROI in 3 months or less, and unlock new growth potential by shifting your most valuable resources (your peoples' time) where it can make the biggest impact.

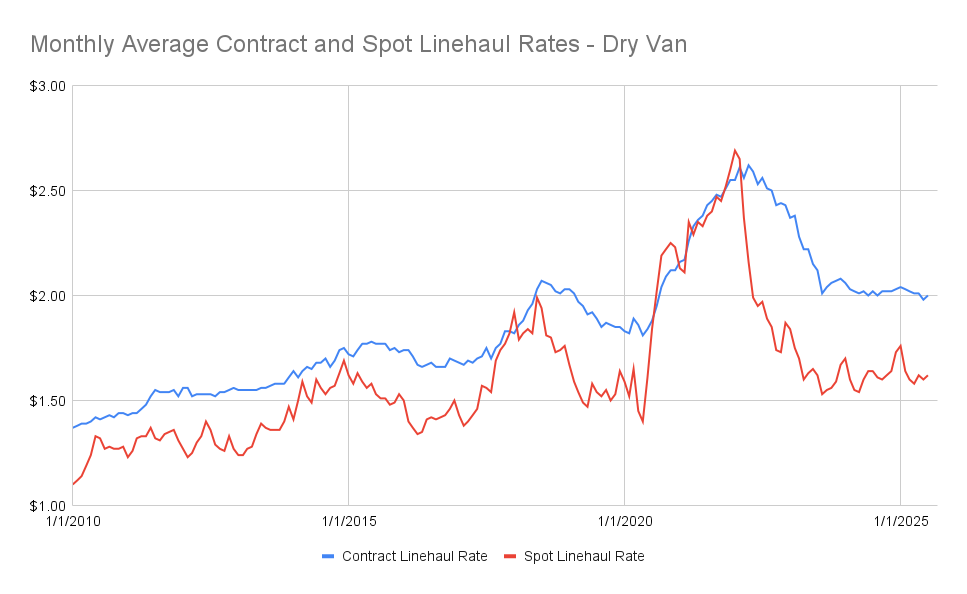

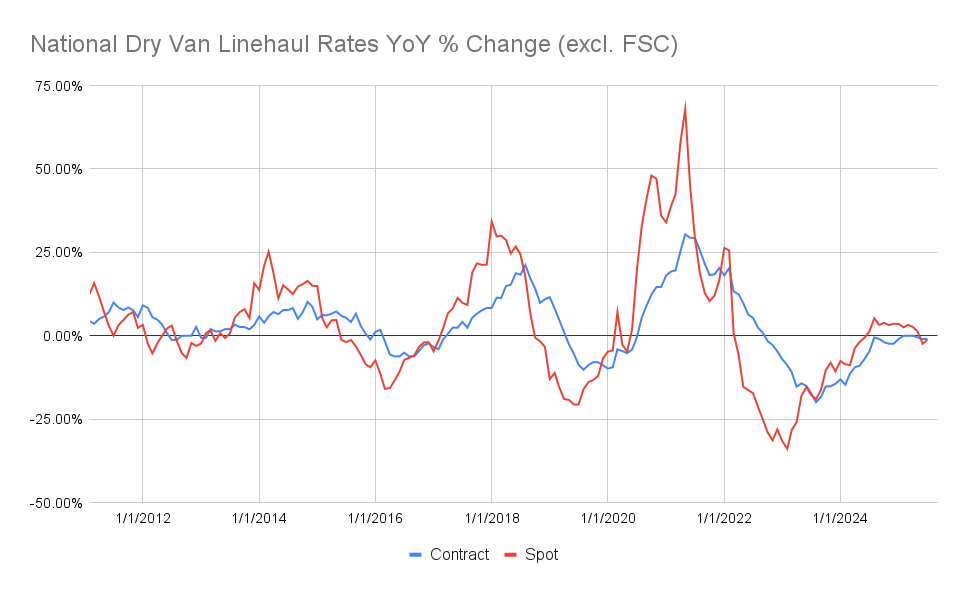

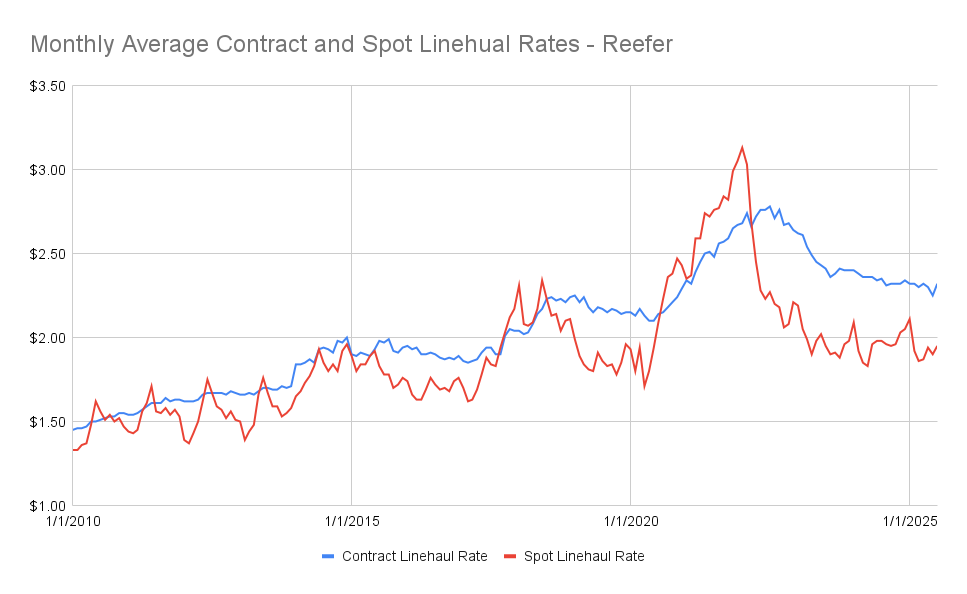

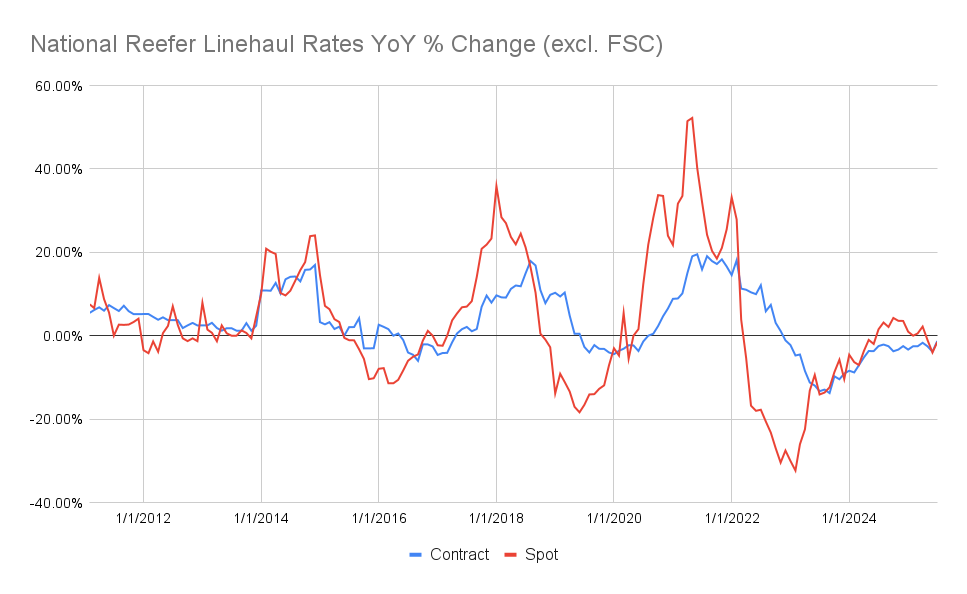

Last but not least, let's check in at our August updated charts for dry van and reefer spot and contract rates.

Dry van has seen some slight gains in recent months but it's still a very slow and steady pace. The gap between spot and contract rates remains wide. Reefer rates have seen some upward rate pressure in recent months both in spot and contract spaces, but overall rates remain down and the gap remains wide.

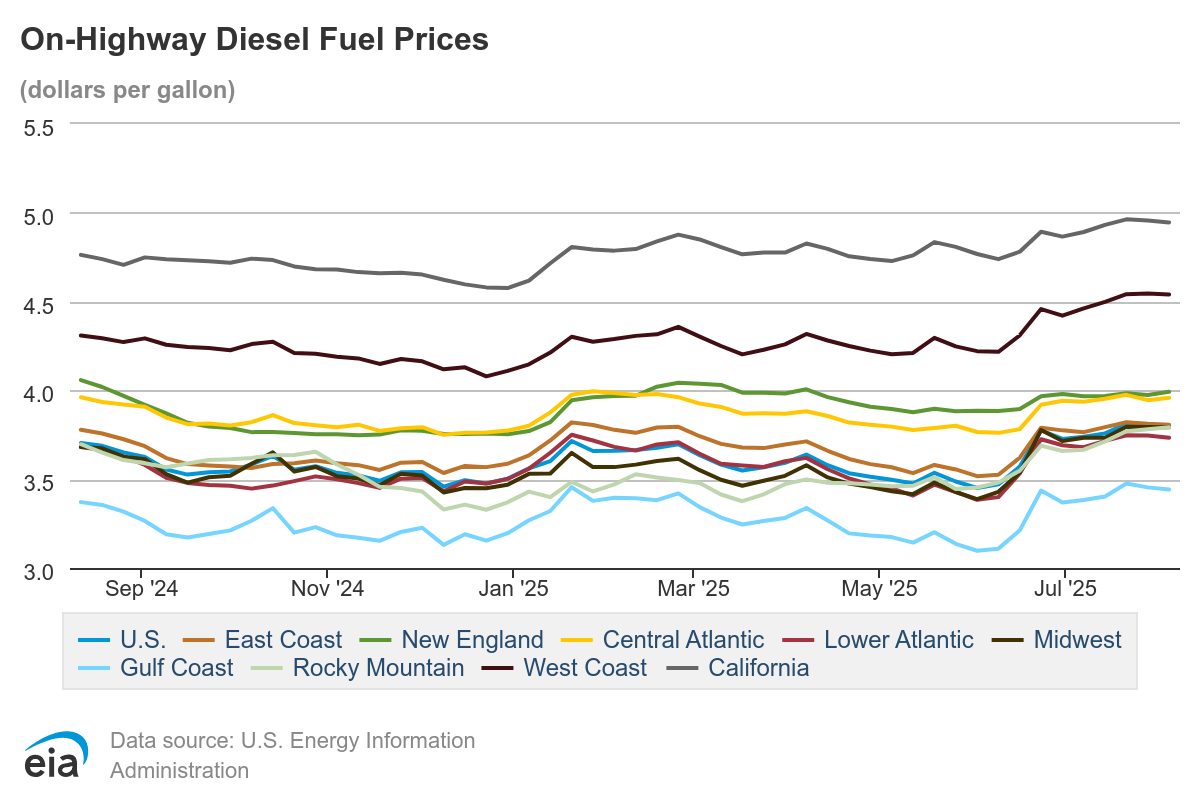

Fuel prices have also seen notable increases in recent months, which puts further pressure on carriers.

Meet Me For Coffee with Samantha Jones seeks to correlate macro-economics to freight markets (just like this Newsletter does) and offers a chance to hear various industry and non-industry experts explain their thoughts on economics and freight markets.

Thank you to our sponsor, Watco Logistics. As a leading 3PL, Watco Logistics provides rail, highway, intermodal, e-commerce and fulfillment, barge, international and cross-border solutions. At the core, Watco Logistics specializes in solving unique supply chain challenges. Learn more about Watco Logistics here!

Check out our Podcast Channels on your preferred platforms!

Save Money On Conferences!

Here is where Samantha is heading next, take advantage of her media sponsorship with these conferences to save $$ on your own registration! Questions about these shows, not sure which ones are for you? Message Samantha!

The JOC Inland Distribution Conference is coming up soon in September! I have a code to save you 15% off your registration! COFFEEINLAND25 https://inland.joc.com/en/register Want to know if Inland is for you? Check out this video!

Discount to save $200 on your Manifest: The Future of Supply Chain & Logistics registration! ManifestVegas.com/MeetMeForCoffee

Thank you so much for reading and supporting the Truckload Market Update Report, produced by Samantha Jones Consulting LLC. Samantha Jones Consulting focuses on helping companies in the logistics industry better brand and sell their services to create sustainable revenue growth, and support their company growth goals!

We love Feedback, if you have questions, comments, suggestions, or are interested in sponsorships or partnerships, please email samantha@connectsjc.com to connect!

Make sure you subscribe to the Newsletter to receive the monthly update, and please share this with a friend who can also benefit from reading! As always, Samantha's work is free and created with the intent to add value to the transportation industry.