This is the final edition of the year, and what a year it has been. It is safe to say 2025 did not unfold the way many of us expected. I went back to my last edition of 2024 to revisit what I believed was ahead. Here is what I wrote:

“If I were to skip straight to my own take, I’d say growth might be back-loaded into the latter half of 2025. Even then, the recovery may take longer to gain momentum than previously expected. This year’s peak season, marked by reports of declining LTL tonnage and a lack of significant disruption in FTL rates, could set the tone for 2025 as well.

If the market maintains supply equilibrium, with minimal carrier exits over the next six months, combined with a still “uncertain” macroeconomic landscape, it’s hard to see 2025’s peak season being drastically different from what we’re experiencing now. But the 2025 peak could also be built into what most economists think will be a strong year of growth in 2026.

As we look ahead to 2025, the path for rate cuts appears increasingly cautious. A slowing economy, uncertainty around the neutral Fed funds rate, and potential shifts in economic policy under a new Federal administration are all contributing factors. While the Fed maintains a bias toward lowering rates, it has signaled a measured approach, with longer intervals between adjustments likely. Strong economic growth, a resilient labor market, and persistent inflation variability suggest that December could bring a rate cut—but it may be the last one we see for some time. All eyes are on the ISM’s PMI for the next several months as we look to see impactful improvements in domestic manufacturing to help bring the freight markets back to life.”

Overall, I am not disappointed in how I characterized the year ahead. It did take longer for the market to show any real momentum, and even then, that momentum did not hold. Supply equilibrium largely remained intact, uncertainty persisted, and this year’s peak season feels only marginally different from last year’s. The Fed remained cautious on rate cuts, and despite early signs of improvement, the ISM did not deliver the sustained progress many hoped to see by year's end.

The word missing entirely from my closing thoughts last year: tariffs.

And then 2025 began, and tariffs quickly became the defining theme.

The uncertainty surrounding tariff policy was the single factor that disrupted nearly all predictability for 2025. Uncertainty became the prevailing headline. As we look toward 2026, tariffs remain central, but affordability is beginning to compete for equal attention.

I listened to Jerome Powell’s press conference yesterday following the announcement of the 0.25 bps cut. He stated with confidence that he believes inflation is under control, or well on its way to being under control, in categories not affected by tariffs. He also noted that the inflationary effects of tariffs on goods are likely to manifest as a one-time price adjustment that peaks in Q1 2026, remains elevated for nine months, and then recedes. This, of course, assumes no additional tariff actions that would increase these impacts. If this outlook proves accurate, it suggests we still need another whole year for tariff-related uncertainty and inflationary pressure to play out. Not to mention, there's a Supreme Court Case in the balance, and a decision to reverse any part of the tariffs would add more uncertainty about how things will shake out for businesses and consumers.

As I think about 2026, I want to share my expectations here so we can revisit them next December. Afterward, I will also share perspectives from individuals whose insight I value deeply, including guests from the Meet Me For Coffee podcast who contributed thoughtful commentary on the economy and freight markets throughout 2025. I hope you find value in our collective year-end reflections.

Last year, as we closed out 2024, I believed the story of 2025 would be centered on interest rate cuts driving economic activity through increased investment in domestic manufacturing, construction, real estate, and borrowing. What I did not anticipate was the magnitude of the tariff impact. Tariffs alone created enough uncertainty to keep interest rates higher than many of us expected by the end of 2025, by presenting the most substantial headwind in the fight against inflation.

Just this week, Keith Prather discussed tariffs on my podcast, and Jerome Powell answered several insightful questions about their ongoing impacts. I believe we are nearing the point where tariff effects are beginning to recede, but we are not there yet. Tariffs will remain a meaningful driver of uncertainty heading into 2026. I find myself more pessimistic than usual when it comes to the freight markets, and I genuinely hope I am wrong. While I hope the economy outperforms expectations, my outlook for 2026 remains conservative.

Here are the key areas I am watching:

Q1 Tax Return Stimulus: What will the effects be? Could they be inflationary? I expect the Fed will want to observe this dynamic before making further decisions.

Tariff-related inflation, I expect the inflationary peak from tariffs in Q1 2026, followed by a gradual settling throughout the year as prices adjust. By Q4, many experts anticipate inflation returning to the 2 percent target or slightly above.

Domestic economic activity: I anticipate a modest uptick by Q2 2026, with slow, steady growth through Q3. Some forecasts suggest activity may cool by Q4, and many are calling for slower GDP growth in 2027.

Truckload rates, I expect contract rates to remain in the single-digit increase range throughout 2026, particularly given their tendency to lag spot rates. The spot market needs demand stimulus, and although I am optimistic about some tightening in Q2 and Q3 as demand improves, I do not expect dramatic spikes or rapid rate surges.

Truckload supply, I expect ongoing pressure on supply over the next six months, with additional capacity potentially exiting the market. However, despite continuous carrier closures, we have yet to see significant effects on rates. If demand rises sharply, supply will struggle to keep pace. If demand increases more gradually, as I anticipate, I do not expect a substantial imbalance between supply and demand.

I welcome your thoughts as well.

Now, moving on to the contributions from some of my favorite economic and freight market voices:

David Spencer, VP of Market Intelligence at Arrive Logistics offered this when asked for a quote:

“As we enter 2026, uncertainty remains central to the outlook. The stronger-than-usual seasonal rate response in late Q4 suggests that supply and demand tightened through 2025, even amid weak demand. This points to ongoing supply contraction, and with low equipment orders and increasing regulatory pressure ahead, capacity will likely remain at risk in the new year. It is still unclear whether tariff-driven inflation has fully reached consumers, but if it does, it could weaken goods consumption and add further downside pressure on the market. Conversely, any demand growth—whether driven by economic stimulus or improved investment conditions—could test the market’s ability to supply capacity and potentially trigger a more sustained disruption. In short, I believe the direction of demand in 2026 will determine the market's direction.”

Ken Adamo, GM Shipper and Chief of Analytics at DAT Solutions, offered his thoughts.

“Honestly, I think it's anyone's guess where 2026 will land. Without a meaningful uptick in demand, any supply-driven recovery will be tepid. There are way too many regulatory and policy unknowns, including non-domiciled CDLs, ELP, broker financial liability, etc. We're hearing from shippers that bid season is a little more competitive than the last two years, but consensus is around 2-5% increase in contract rates. My overall feeling is that we'll need to wait until the spring shipping season picks up to get a clearer idea of where 2026 will finish.”

Mazen Danaf, Principal Economist at Uber Freight, provided the following commentary.

"The supply outlook looks more certain than demand, as we are expecting a significant capacity decrease in 2026. A few factors drive this:

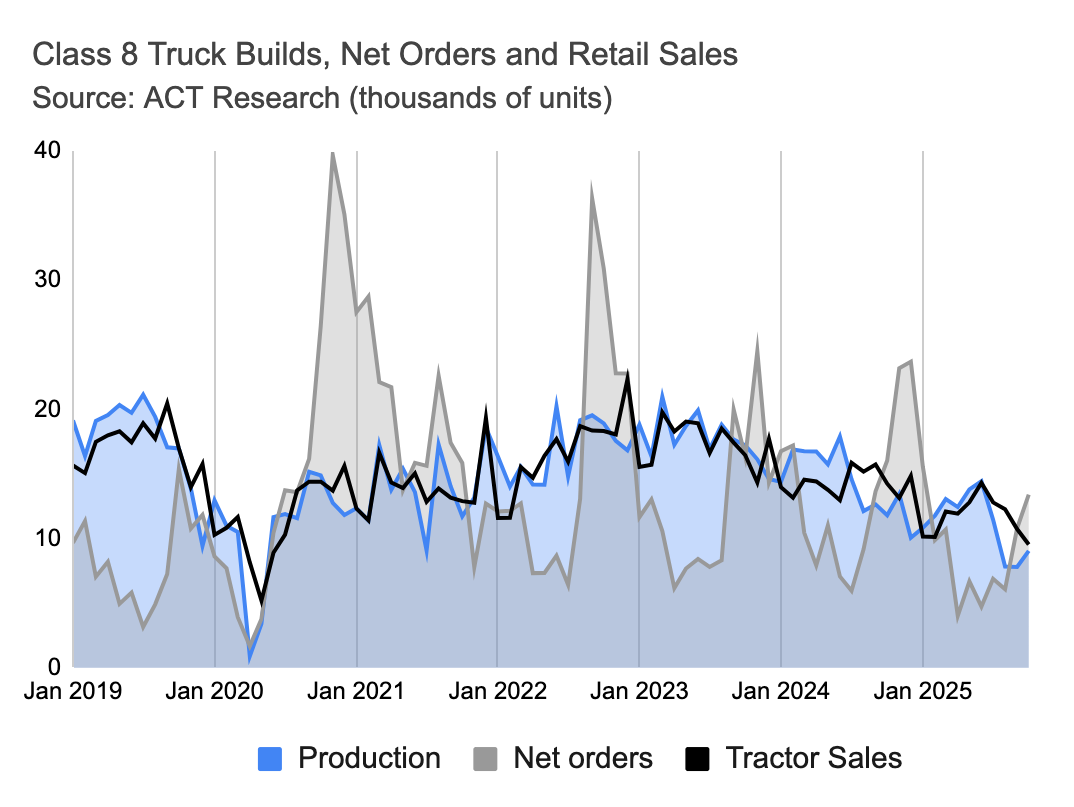

Capacity reduction, previously concentrated among smaller fleets, is projected to shift to larger fleets in 2026. The peak tractor ordering season has begun, but it appears significantly weaker than prior seasons. Tractor orders are down 16% y/y and 23% year-to-date compared to 2024. This trend is mirrored in sales and production, with tractor sales dropping 33% and production declining 23% y/y.”

Dry van trailer order activity showed similar trends, dropping 20% year-over-year. While trailer sales increased 8% year-over-year due to easier comparisons, production decreased 4% year-over-year.

In addition, if the FMCSA regulation on non-domiciled carriers (currently being challenged in court) passes, it could remove 200,000 drivers from the market, leading to a more severe capacity crunch that extends beyond small fleets. We still don't know if this will pass, and the FMCSA data has not yet shown any effect on the carrier population.

The demand outlook is more uncertain and depends on factors such as tariff policy and the Federal Funds Rate. So far, we have not seen any signs of an imminent demand recovery, suggesting freight volumes will likely remain weak in 2026.

We have also seen mortgage rates remain high, indicating no recovery in sight for the housing market. This signals weakness in associated sectors like furniture, appliances, home supplies, and building materials.

Looking across the industries we track in our shipments (retail, packaging, wholesale, manufacturing, and food/CPG), only retail and Food/CPG are performing well, while all others are showing y/y decreases. In addition, we started seeing signs of weakness in the Food/CPG industry in the recent months."

Jason Miller provided his thoughts on manufacturing and trucking rates heading into 2026.

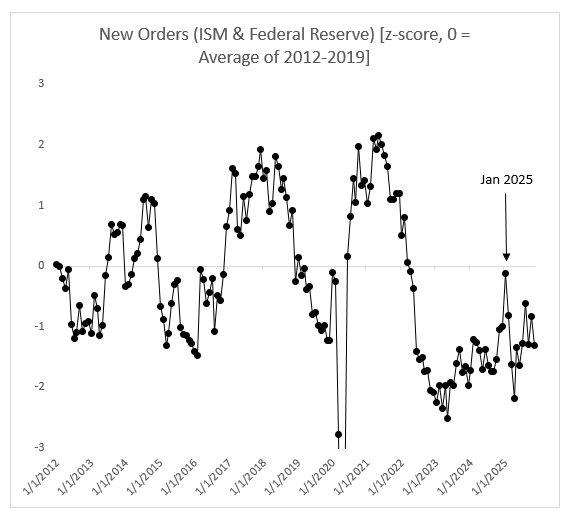

"I finished compiling ISM's manufacturing data with the FRB manufacturing data, and November was a rough month. Given that the 5-bank aggregate FRB data has nearly 2x the standard deviation of the ISM data for new orders, I convert the 5-bank aggregate and ISM new orders data to z-scores (where the mean and standard deviation are from 2012-2019 to avoid the COVID lockdown outliers) and then average the two z-scores. As such, a reading of 0 is neutral for what we saw from 2012 to 2019. All data are seasonally adjusted. November came in at -1.3 (ugh). Looking at each metric, ISM is about -1.6 versus -1 for the FRB, which makes sense given ISM's respondents are likely larger manufacturers with more international exposure per Fort (2023). Looking ahead over the next several months, I'm not sure where we'll see a surge in demand for manufactured goods.”

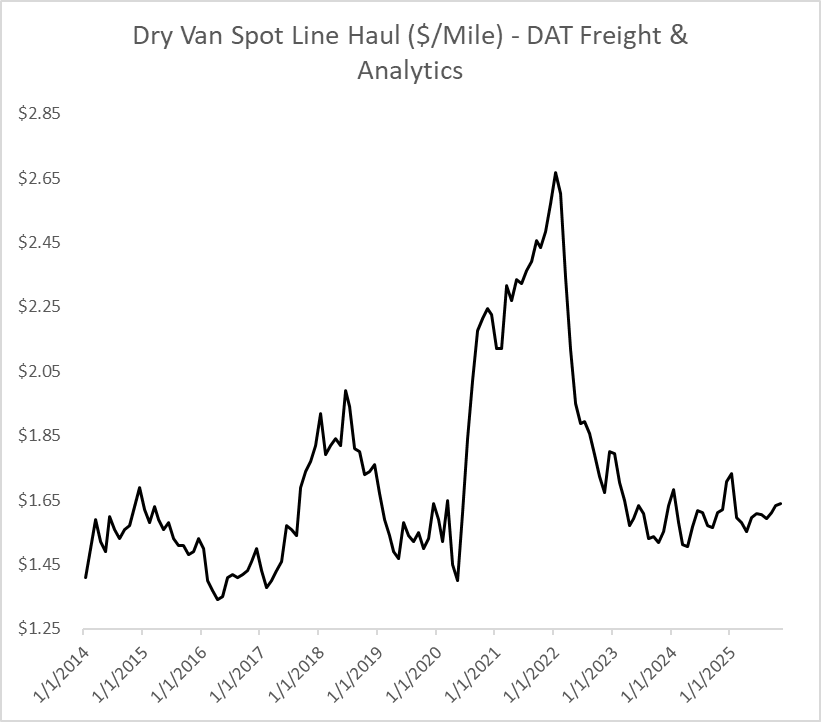

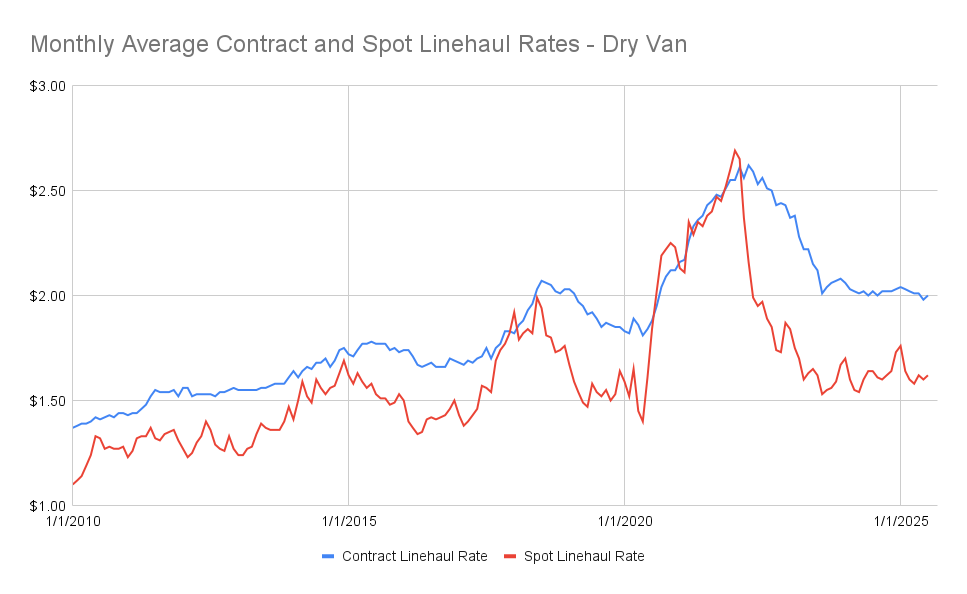

Focusing on the truckload sector, dry van rates have remained effectively flat since Q2 2023. We see dry van rates underperforming relative to most prior years (certainly worse than in 2023 and 2019, for example).

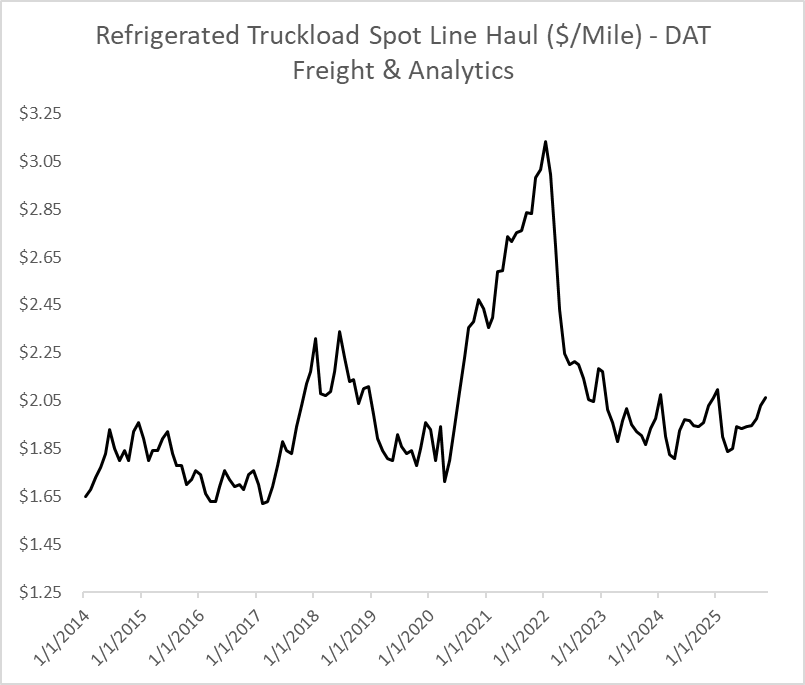

Likewise, the November uptick in refrigerated TL spot rates in November was a bit of an underperformance relative to last year.

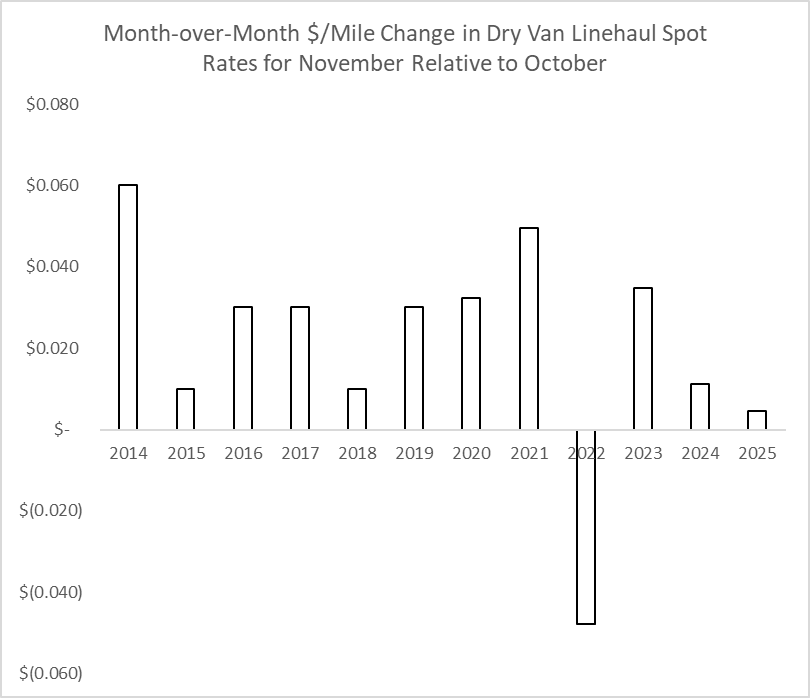

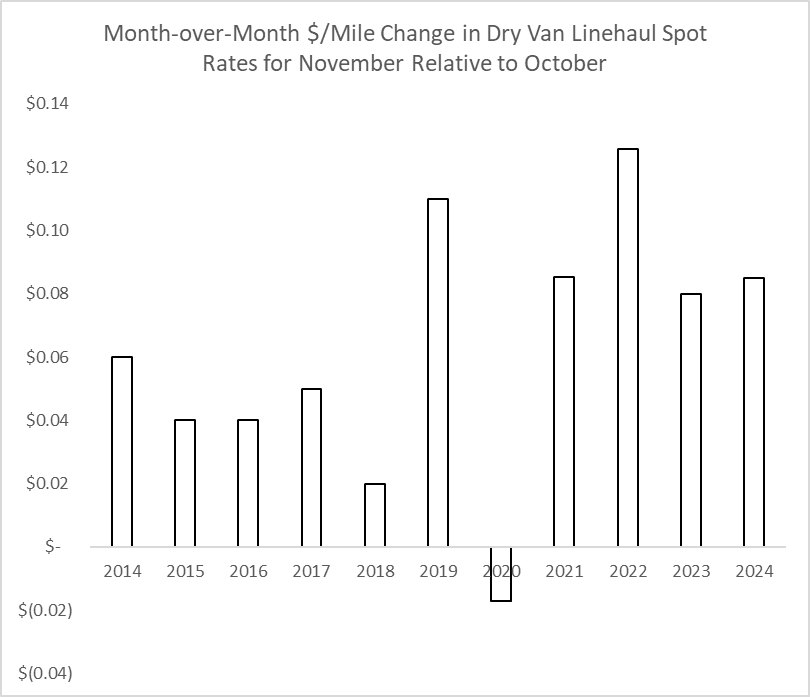

All told, I'm not very optimistic about the next few months from a demand standpoint. December has some big shoes to fill in the dry van TL spot market. In the past few years, we have seen DAT's fuel-adjusted spot rates increase by $0.08 per mile from November to December. That's a hefty ask after November's underperformance.

A huge thank you to BiggerPicture for sponsoring this month's newsletter! BiggerPicture focuses on helping shippers, brokers, and carriers maximize operational productivity by reducing appointment scheduling time by an average of 80%. Achieve full ROI in 3 months or less, and unlock new growth potential by shifting your most valuable resources (your people's time) where it can make the most significant impact.

One of my favorite independent economists, Matthew Klein, Founder of The Overshoot, responded to my request for his thoughts on the economy heading into 2026 with the following thoughts.

"The two most significant changes in the U.S. economy over the past few years have been the improvement in household balance sheets and the swings in net immigration from about +1 million people/year before the pandemic to a peak of around +3 million/year in 2023-2024H1 to something currently below zero, after accounting for deportations and voluntary emigration.”

According to data collected by the Federal Reserve, Americans across the income distribution are substantially more affluent now than they were before the pandemic. Both in absolute terms and relative to their incomes, they have more savings, own more durable goods, have much higher home equity, and owe less in debt. While higher interest rates have affected home buying, overall consumer spending has been far less affected, presumably because households have been able to finance more of their spending with income rather than credit.

Whether that continues depends on the health of the job market, which, so far, has held up despite an apparent weakening over the past 12-18 months. The net number of payroll jobs added or subtracted each month has not been a reliable indicator of the business cycle. More people coming in means more spending and more workers, with the two effects tending to cancel out in terms of wages and inflation. Similarly, fewer people coming in means slower growth in aggregate spending and employment. Still, the recent swing from net immigration to net emigration has not (for the most part) led to meaningful changes in average worker productivity or inflation. The apparent slowdown in job creation is therefore misleading for understanding the economy's health.

More importantly, the share of Americans aged 25-54 with a job has held steady at its multi-decade high for the past 2.5 years, while weekly data on unemployment insurance also imply that people have not been losing jobs. These data are also consistent with the fact that the typical worker's pay has continued to rise about 1-1.5 percentage points faster (annualized) than in the period before the pandemic. If the job market had seriously weakened, pay growth would have decelerated. There has been a notable slowdown in hiring, which has raised the jobless rate for prospective workers under 25. But the impact on the rest of the economy is relatively small, since that cohort has far fewer people than the 25+ cohort. Younger workers are also paid less than the average, and therefore spend less.

The U.S. manufacturing sector has been in the doldrums since before the pandemic. The Fed recently revised down its production estimates, implying no growth since mid-2021. Changes in government policies, including tariffs, regulations, and subsidies, have all been unhelpful. Still, the larger picture is that demand for manufactured goods in many of the world's other major economies has been depressed. At the same time, the dollar's exchange rate, particularly relative to the Chinese yuan, has made it harder for U.S. producers to maintain market share. Some U.S. manufacturing seems to have responded positively to tariffs, particularly output of primary metals, but even that has been insufficient to bring production back to the levels of mid-2022."

And lastly, an economic voice I admire that I did not solicit for a quote recently published some key takeaways I wanted to include as well:

Jan J.J. Groen wrote in his recent publication:

"The September Personal Income and Outlays report provides a good insight into the U.S. consumer as well as inflationary pressures in the future. This note presents some of these insights. Note that the release of this report was delayed to Friday, December 5, owing to the earlier shutdown of the Federal government.”

Key takeaways:

Speaking of the Fed's rate cuts, here is the Fed's decision from yesterday. I listened to the press conference and added some of my takeaways.

The Federal Reserve FOMC Statement that was released on Wednesday:

"Available indicators suggest that economic activity has been expanding at a moderate pace. Job gains have slowed this year, and the unemployment rate has edged up through September. More recent indicators are consistent with these developments. Inflation has moved up since earlier in the year and remains somewhat elevated.”

The Committee seeks to achieve maximum employment and a 2 percent inflation rate over the longer run. Uncertainty about the economic outlook remains elevated. The Committee is attentive to the risks on both sides of its dual mandate and judges that downside risks to employment have risen in recent months.

In support of its goals and in light of the shift in the balance of risks, the Committee decided to lower the target range for the federal funds rate by 1/4 percentage point to 3-1/2 to 3‑3/4 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee is firmly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures, inflation expectations, and financial and international developments.

The Committee judges that reserve balances have declined to ample levels and will initiate purchases of shorter-term Treasury securities as needed to maintain an abundant supply of reserves on an ongoing basis.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Susan M. Collins; Lisa D. Cook; Philip N. Jefferson; Alberto G. Musalem; and Christopher J. Waller. Voting against this action were Stephen I. Miran, who preferred to lower the target range for the federal funds rate by 1/2 percentage point at this meeting; and Austan D. Goolsbee and Jeffrey R. Schmid, who preferred no change to the target range for the federal funds rate at this meeting."

Most reporters, economists, commentators, etc., agreed that less important than the cut itself was the tone Powell would take in the release and in questions, and how many members would vote for no change. Overall, stock markets seem pleased with the Fed’s outlook, and there were definitely some reasons for encouragement.

As I listened to the press conference, I took some notes, bulleted here in no particular order or fashion:

Rates

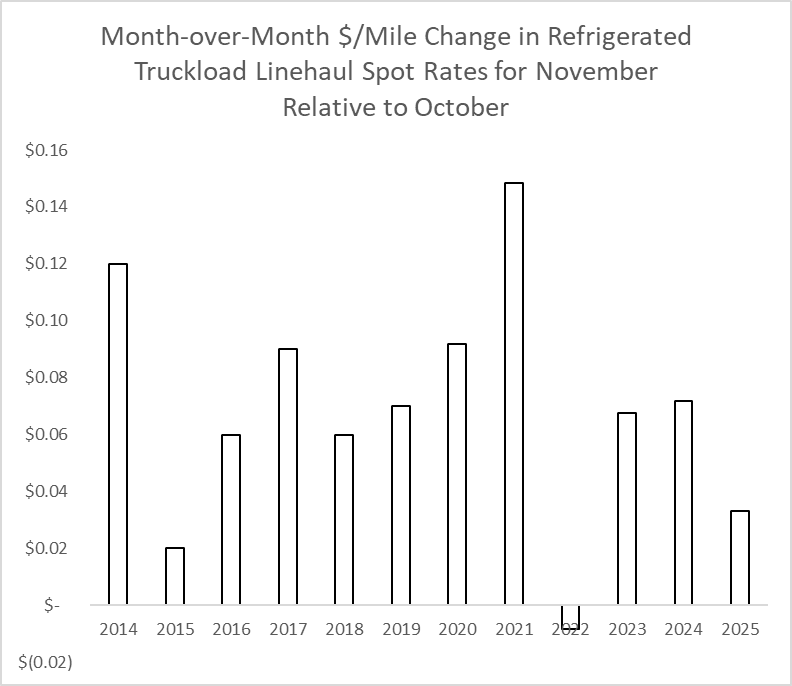

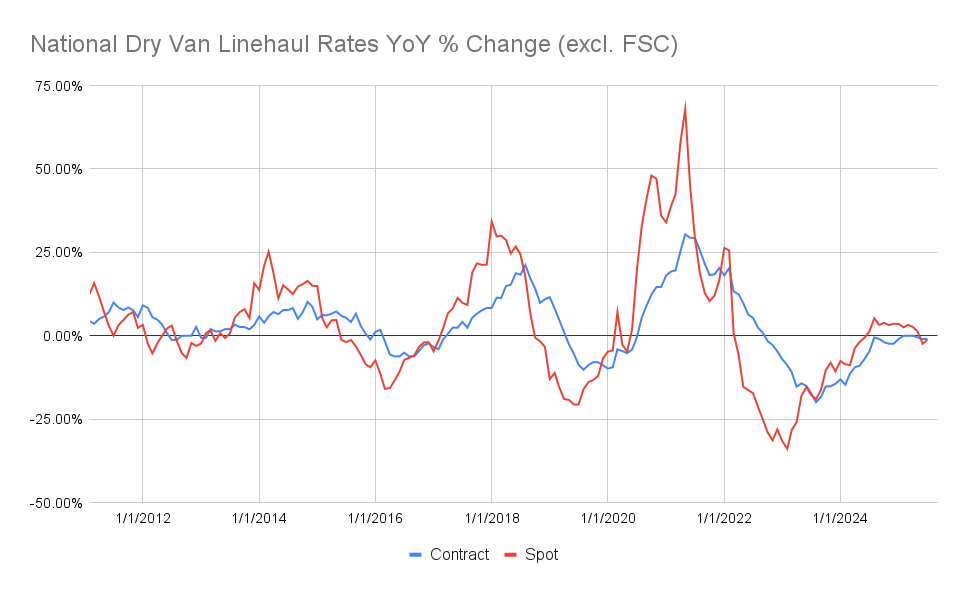

Here are our usual charts, updated through the end of November with DAT data!

Credit: DAT Freight & Analytics

Credit: DAT Freight & Analytics

Credit: DAT Freight & Analytics

Credit: DAT Freight & Analytics

That's all she wrote for 2025! Thanks for reading. Let's see how these thoughts hold up throughout the year! If you are not already a subscriber to the Newsletter, please subscribe! If you don't always see these in your LinkedIn notifications email or on LinkedIn the way you'd like, shoot me a message, and I can add you to our email subscription list as well!

Meet Me For Coffee with Samantha Jones seeks to correlate macroeconomics with freight markets (just like this Newsletter does) and offers a chance to hear various industry and non-industry experts share their thoughts on economics and freight markets.

Thank you to our sponsor, Watco Logistics. As a leading 3PL, Watco Logistics provides rail, highway, intermodal, e-commerce and fulfillment, barge, international, and cross-border solutions. At the core, Watco Logistics specializes in solving unique supply chain challenges. Learn more about Watco Logistics here!

Click to Learn More!

Check out our Channels on your preferred platforms!

Here is where Samantha is heading next, take advantage of her media sponsorship with these conferences to save $$ on your own registration! Questions about these shows, not sure which ones are for you? Message Samantha!

Discount to save $200 on your Manifest: The Future of Supply Chain & Logistics registration! ManifestVegas.com/MeetMeForCoffee

Thank you so much for reading and supporting the Truckload Market Update Report, produced by Samantha Jones Consulting LLC. Samantha Jones Consulting focuses on helping companies in the logistics industry better brand and sell their services to create sustainable revenue growth and support their company growth goals!

We love Feedback. If you have questions, comments, suggestions, or are interested in sponsorships or partnerships, please email samantha@connectsjc.com to connect!

Make sure you subscribe to the Newsletter to receive the monthly update, and please share this with a friend who can also benefit from reading! As always, Samantha's work is free and created with the intent to add value to the transportation industry.