After months, honestly YEARS, of having very little to say about full truckload rates in the “Rates” section of this newsletter, I suddenly have a lot to say this month. Pricing has moved dramatically, and I expect volatility to continue this week as we enter DOT Week. The 2026 CVSA International Roadcheck (commonly known as DOT Week or DOT Blitz) is scheduled for May 12–14, 2026. During this 72-hour period, law enforcement agencies across the U.S., Canada, and Mexico will conduct intensified inspections, with a particular focus on ELD compliance and cargo securement. Expect heightened inspection activity, potential carrier delays, and increased spot market volatility.

But before diving too deeply into rates, let’s stick to our usual structure and start with the broader economic backdrop shaping freight markets. Unlike rates, not much has materially changed on this front — with the obvious exception of energy and fuel prices. At the moment, these are arguably the largest threat to interest rate cuts and continued progress on inflation. Fuel prices remain elevated due to the ongoing conflict in Iran and the closure of the Strait of Hormuz. As David Kelly, Chief Global Strategist at JP Morgan, wrote in a recent publication:

“the Iran war has now entered its third month, with a temporary ceasefire but also a U.S. blockade of Iranian ports, a de facto Iranian blockade of the Strait of Hormuz and no sign of any resolution of the underlying nuclear issue. We continue to believe that the U.S. will eventually accept an agreement by which the Strait is reopened before more extended negotiation on the nuclear issue. However, timing is important here. Every day the Strait is closed, global oil inventories fall. This has actually had a somewhat muted impact on oil prices so far, since the world entered 2026 with near-record high stockpiles of oil and oil products. These inventories fell rapidly in both March and April and, if this continues for a few months more, then oil prices could move much higher. However, before this fully plays out, it should become a more urgent issue for the U.S. administration due to the political cost of fast-rising gasoline prices and our baseline view is one in which traffic through the Strait resumes close to normal patterns within the next two months, with global oil prices falling sharply although not to pre-war levels. “

Consumers are feeling the impact directly at the pump, and high gasoline prices have historically been an emotional pressure point for voters. It’s not in the administration’s interest to prolong additional financial strain on U.S. consumers, which is why many economists believe the U.S. will ultimately need to find a path toward reopening the Strait sooner rather than later.

That said, there is still meaningful risk that this situation drags on longer than expected, or that oil supply takes more time than anticipated to normalize even after the Strait reopens. The longer global trade flows remain disrupted, the more prolonged the downstream effects are likely to be, even after operations resume. For now, I expect elevated fuel prices to remain with us throughout the summer.

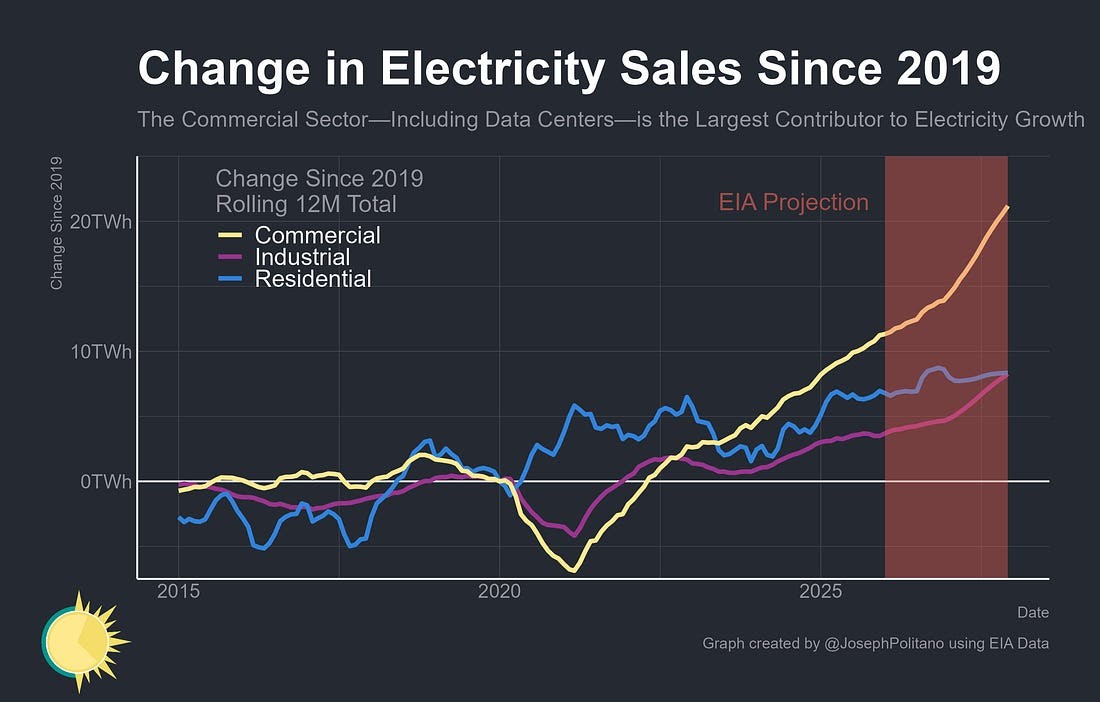

Has anyone else noticed a meaningful change in their electric bill? I definitely have. I’m guilty of putting my utilities on autopay and rarely giving them much attention, but over the last two months my electricity bill has reached levels I’ve never seen before. At first, I assumed something had to be wrong. Instead, it appears growing electricity demand is beginning to meaningfully filter down into household expenses.

That’s why I was particularly interested in Joseph Politano ’s latest piece on this exact topic. In short, households are now facing a combination of rising electricity costs and elevated gasoline prices simultaneously. While consumers have largely adjusted to inflation across many categories over the last few years, utilities and fuel are harder expenses to mentally absorb because they are highly visible, unavoidable, and hit monthly household budgets directly.

If you find this snippet interesting, I highly recommend reading the full article linked here.

“America has entered another era of electrification—US power consumption has risen more in the last two years than over the previous 15 combined. Yet this hasn’t been nearly enough to meet demand, with electricity prices also rising more over the last 4 years than the prior 14. Demand from AI, heavy industry, heating, and transport is driving load growth but also outstripping growth in power infrastructure—leaving America with an increasingly large electricity gap that’s driving up prices. Projections from the US Energy Information Administration (EIA) expect generation to accelerate slightly over the next two years, growing another 4.6% in total, but that’s still not quick enough to close the gap or prevent further price appreciation. “

The Iran conflict is pushing fuel prices higher, but what’s driving electricity costs upward? Increasingly, it appears to be the AI revolution. The explosive growth of AI technology has created enormous new infrastructure demands. Alongside the rapid buildout of data centers comes the equally massive need for electricity to power them.

If you read the article referenced above, you may have been just as surprised as I was to learn that solar has now become the fastest-growing source of alternative energy in the United States, particularly when paired with rechargeable battery storage systems. That trend alone says a lot about where energy demand forecasts are heading over the next decade.

Speaking of AI, I believe it’s one of the reasons economists have consistently struggled to accurately forecast the economy over the last couple of years. Entering 2026, many economists were predicting elevated recession risks, slower economic growth, labor market deterioration, and broader economic weakness due to the numerous headwinds facing the economy. Yet once again, the U.S. economy has remained surprisingly resilient, and in several areas has even exceeded expectations. That resilience is especially notable now with Q1 U.S. GDP posting a 2% growth rate.

Another factor is that tariffs appear to have had a smaller inflationary impact than many originally expected, particularly in light of the latest developments and easing tariff pressures.

So far, I think we can credit several factors for the economy’s continued resilience:

Even with continued economic growth, that does not make the Federal Reserve’s job any easier. The labor market has managed to remain relatively stable, but inflation has refused to return to the Fed’s target range over the last year. Now, several inflationary headwinds appear to be building again.

At the same time that tariff-related inflation concerns are beginning to ease, supply-side shocks are once again placing upward pressure on inflation. Gregory Daco addressed this dynamic in a recent publication:

“The broader challenge is that the US economy is confronting the price of growth. A sequence of supply shocks—from trade policy and tariffs to demographics and immigration, and now the Middle East conflict—continues to put upward pressure on inflation while weighing on growth. As Powell noted, policymakers have been operating in a “situation of supply shocks… for six years.” To that list, we would add the positive shock from a likely AI-led technology cycle. This environment of layered supply shocks complicates policy calibration and reinforces a wait-and-see bias. Looking ahead, while we continue to expect easing inflation in the latter part of 2026 alongside further softening in labor market fundamentals, we no longer anticipate a rate cut in December. Powell’s acknowledgment that market’s interpretation of the Fed’s reaction function is broadly accurate reinforces the view of a Committee on hold through the remainder of the year.“

Why might inflation ease in the latter part of 2026? There are several reasons. First, oil prices will hopefully decline as the U.S. government works toward ending the closure of the Strait of Hormuz. Second, the administration appears unlikely to pursue new tariffs significant enough to trigger another major inflationary shock. Third, with only 0–1 interest rate cuts expected for the remainder of the year, borrowing activity and consumer demand are unlikely to accelerate meaningfully.

I’ve covered tariffs extensively in prior newsletters, but as a quick update: it increasingly appears that the peak of the recent tariff push may already be behind us. After the Supreme Court struck down the IEEPA tariffs in February, the administration quickly announced a new 10% tariff under alternative legal authority and even floated the possibility of raising it to 15%. However, the 15% increase never materialized, and the 10% tariffs continue to face legal challenges in the courts.

Even if the courts ultimately uphold the 10% tariffs, overall tariff pressure has already moderated. Tariff revenue accounted for roughly 11% of imported goods in late 2025, but by March 2026 that figure had fallen to 7.3%. While the administration has stated that it intends to replace the lost tariff revenue through alternative tariff mechanisms, that outcome appears increasingly unlikely in an environment where inflation remains a primary economic concern. Because of this, many economists now expect the effective tariff rate by the end of 2026 to be materially lower than it was at the end of 2025.

David Kelly also echoed Gregory Daco’s outlook regarding near-term inflation pressures followed by easing inflation over time:

“On Inflation, some further heating up is likely into the summer but then price increases should recede. In March, the Fed’s preferred measure of inflation, the personal consumption deflator, rose by 3.5% year-over-year and we expect this to rise to 3.9% year-over-year for May. However, thereafter, we expect inflation to drift down due to falling oil prices, lower tariff rates and a continuing slide in shelter inflation reflecting the impact of weaker demographics on rents. Inflation, as measured by the PCE deflator should fall below 3.0% year-over-year by December and below 2.0% year-over-year by April 2027.”

And speaking of the near future, Gad Levanon , who has now appeared on my podcast twice, both times discussing AI and its economic implications, recently published an incredibly insightful article on the short- and long-term impacts the AI revolution is likely to have on the U.S. economy. Here are a few of my favorite excerpts, but I strongly encourage you to read the full piece.

As a business man or woman operating in the U.S. today, it is becoming increasingly important to understand where AI is headed and how profoundly it is likely to impact nearly every aspect of corporate America. Whether that impact ultimately proves more disruptive or more productive in the near term, and the long term, remains one of the biggest economic questions facing businesses today.

“The next 12 months split cleanly. AI is the story. Policy is noise.

That is not where most forecasters are. The consensus view going into 2026 is for growth to slow modestly toward trend. Recession risk is often mentioned. Policy — tariffs, immigration, federal layoffs — is treated as the swing variable. AI is acknowledged as a long-run productivity story but not as a near-term macro driver. I think that framing has the wiring backwards. The forces consensus treats as decisive in the next 12 months are largely spent. The force consensus treats as long-run is already carrying GDP in the quarterly data. The 2025 precedent is the tell: the same forecasters who expected a self-inflicted recession last year missed because they underweighted the AI investment cycle and the productivity acceleration. Repeating that mistake in 2026 is the central forecasting risk, not avoiding it.

AI advances on three fronts at once.

Capability keeps improving. Adoption is accelerating — 2025 was the year firms experimented; 2026 is the year they deploy. And actual GDP keeps catching up to AI-driven potential.

Capex isn't just continuing, it's expanding. Hyperscaler guidance for 2026 is bigger than it was six months ago. Power, chips, construction — all running hotter. AI investment is now visibly carrying GDP in the quarterly data. Q1 earnings did the rest: earnings growth and net margins are both running at multi-year highs.

Adoption is the bridge from buildout to broad productivity. As many firms move from experimentation to deployment, channels 5 through 8 — workflow redesign, lower task costs, reallocation, eventually lower prices — start showing up in the macro data.

Job growth remains very weak. Unemployment among recent college graduates keeps rising — entry-level white-collar work is where substitution is fastest. The wealth channel and a still-falling saving rate carry consumption through the year.

The 2025 headwinds are largely exhausted. Federal workforce cuts have run through the data. Tariff price effects are absorbed. Border crossings have been near zero for many months, with no further tightening to come.

Iran matters but stays in proportion. The energy shock is a tax on the expansion. The economy has shown it can absorb the disruption.

The main story is AI, not Trump.”

The first thing worth noting is that freight volumes have not increased enough to justify the magnitude of the rate increases the industry is currently experiencing. As a recent FreightCaviar newsletter pointed out, tightening capacity and rising diesel prices, with diesel being the larger driver, are the primary forces behind the recent surge in truckload pricing.

“Freight volumes barely moved in Q1 (down just 0.3% from last quarter), but what shippers paid to move their goods jumped 12.9% in the same period. Year over year, spending is up 21.8%. That's the largest quarterly cost spike since late 2020, driven not by a demand surge but by capacity tightening and a March diesel price jump. Fewer trucks are competing for the same freight. Tyson Foods CEO Donnie King spelled out the shipper response on Monday: freight costs get passed through to customers.”

Before going fully into rates, it’s worth briefly blending rates and macroeconomics together because the two are becoming increasingly interconnected.

At the moment, fuel costs are being passed through almost entirely across the supply chain. Ocean carriers are passing those increases to shippers, trucking companies are passing them to shippers or brokers, brokers are passing them through to customers, and ultimately many shippers are attempting to push those higher costs onto consumers. Why wouldn’t they? Consumer spending has remained surprisingly resilient despite tariff inflation and broader economic pressures.

However, there is still a meaningful risk that consumers, and corporations, may not remain this price elastic indefinitely. At some point, the market begins pushing back against continuous cost pass-throughs, particularly if economic growth slows while inflationary pressures remain elevated.

Trailers are actually a very relevant example that many of us in this industry can appreciate. Trailer manufacturers were hit hard over the last two years by substantial aluminum and steel tariffs on core manufacturing materials. However, because demand was already weak, with trailer orders running well below historical norms and manufacturers already taking production lines offline due to slowing orders, they delayed price increases as long as financially possible.

Even when prices were eventually raised, it was clear that manufacturers were not passing through 100% of the tariff increases directly to buyers as a pure “tariff tax.” Instead, many absorbed part of the cost pressure internally in order to remain competitive and preserve demand.

Companies across the broader economy are now facing a very similar challenge with fuel costs. The question becomes: how much of these rising transportation costs can businesses realistically pass through to customers, and in which areas, before they begin losing business or reducing demand? The greater a supply chain’s exposure to transportation costs, the more difficult it becomes to strike the right balance between preserving margins and maintaining pricing competitiveness.

As Greg Knowler with S&P Global's Journal of Commerce recently published:

“Maersk’s monthly bunker fuel bill has doubled to $500 million since the war in the Middle East began — and those costs are being recovered “in full” from the carrier’s customers via surcharges and revised bunker formulas, CEO Vincent Clerc said Thursday. But Maersk’s ability to continue that cost recovery will depend on the long-term impact of high energy prices on consumer demand and how the container shipping industry manages growing excess capacity, Clerc told analysts during the carrier’s first-quarter earnings call. “Our concern is a softening of the demand environment and insufficient capacity management across the industry”

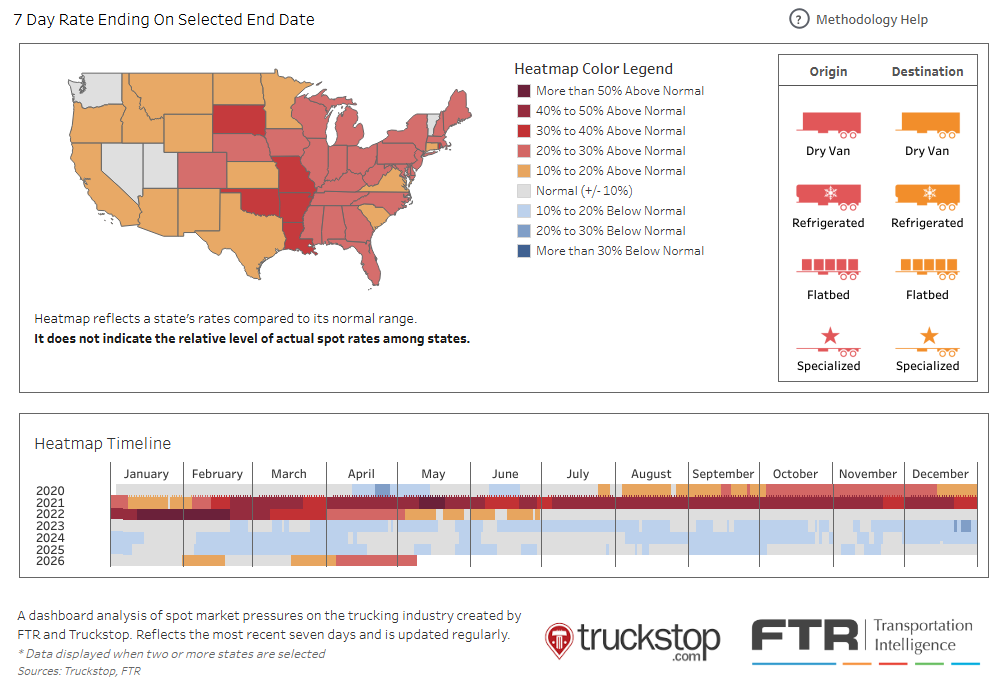

I want to start with these heatmaps. I review these weekly, but have not included them in a market update report in years. The reason is simple, there was nothing interesting about them. For YEARS look at all that blue in the bar charts below? Blue represents rates below normal, and grey is considered normal. We have not touched slightly above normal rates since 2022, until now. The last month has led us into an elevated rate period for the first time in over 3 years.

For Dry Van:

For Reefer:

For Flatbed:

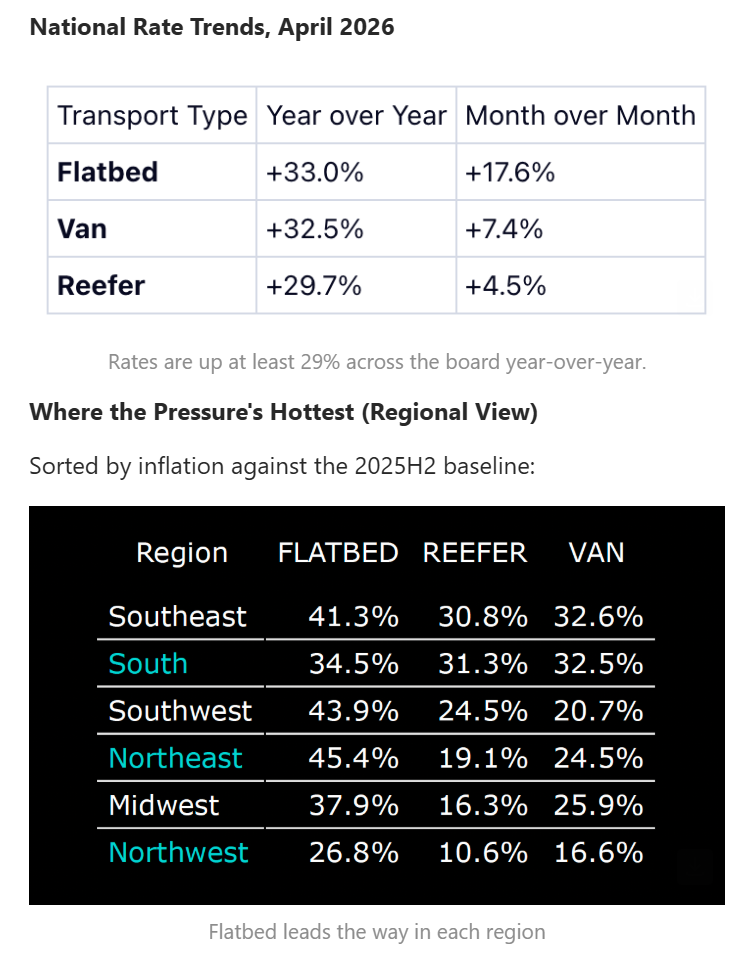

The overall spot market prices are up significantly. This is unsurprising as spot markets can react faster to fuel price increases. As the below mentions, and we need to realize, it’s not possible to say how much of a spot rate is fuel with the data available to us, as spot market rates are mostly “all in” rates, including linehaul and fuel. However, any broker, carrier or shipper you speak with right now will tell you how hard the FSC charts of contract lanes have had to be working these last 3 months.

“The total market broker-posted rate increased by 5.7 cents a mile after rising more than 3 cents in the prior week. All-in broker-posted rates were 32% higher than in the same week last year while rates excluding a calculated surcharge were nearly 26% higher. Although carriers operating in the spot market typically do not receive surcharges, the calculation is a proxy for the portion of the rate needed to offset higher fuel costs. During the current week of the year (week 18), dry van and refrigerated spot rates usually rise while flatbed rates usually fall. Next week almost certainly will bring higher rates for most equipment types due to the annual International Roadcheck roadside inspection event, which is scheduled for May 12-14. As is the case in late June and late December, the week of International Roadcheck is one of a handful of times when rates are guaranteed to rise with the only question being how much.”

To look at this another way, and to break it out by region, I snagged this chart from Triumph Market Insights ’s recent market insights publication:

Graphs help data tell stories. All of us are visual learners to some extent. This graph helps to clearly show why we should be expecting such a strong increase in rates. How much of the jump is fuel vs. tightening supply? That is tough to tell. Some brokers I have spoken with advise there is very little change in the market outside of fuel costs. I suppose this is likely to be industry specific. Some manufacturing or import heavy industries are still down in activity this year, and the trucking companies and brokers serving those sectors have not experienced any rate gains outside of fuel passthroughs.

Last but not least, this ruling is too important to not mention. I will be sure to revisit in July after the final decision, but everyone be paying attention! Below article sourced here.

“Every broker in America is about to find out if the last 30 years of how they've done business is legally defensible. The Supreme Court's decision in Montgomery v. Caribe Transport II is due by end of June, and what comes back could fundamentally change carrier vetting, broker liability exposure, and the cost of doing business in this industry.

Here's what happened. In December 2017, a truck driver named Shawn Montgomery pulled to the shoulder of I-70 in Illinois with a mechanical problem. A tractor-trailer drifted off the road and hit him. Montgomery lost a leg. The load had been booked by C.H. Robinson. Montgomery sued the carrier and the broker.

The question the Supreme Court is now answering: does federal law protect brokers from being sued under state tort law for negligently selecting a carrier?

The numbers behind the stakes:

The legal split that forced SCOTUS to act. Federal circuits have been ruling differently for years. The 7th Circuit said federal law does preempt state negligence claims against brokers. The 9th Circuit disagreed — C.H. Robinson actually lost a similar case there. The 6th Circuit sided against TQL in Cox v. TQL last year. Brokers have been operating under different legal standards depending on which state a load crossed through. The Supreme Court is the only way to settle it.

What the justices signaled. During oral arguments March 4, Justice Sotomayor asked directly: "Why can't brokers be held liable? They're the one putting the driver in the seat." Justice Kavanaugh pushed the other direction — worried that exposing brokers to open-ended liability would force them to only work with large, established carriers, cutting small fleets out entirely.

The Trump administration filed a brief siding with the brokerage industry.

The two scenarios brokers need to game out now:

If the Court sides with C.H. Robinson and upholds federal preemption, state negligence claims against brokers get significantly harder to bring. Brokers continue operating largely as they do today, but carrier vetting practices still face more scrutiny.

If the Court sides with Montgomery and allows state tort claims to proceed, every broker in the country is suddenly subject to 50 different state liability standards. Carrier selection decisions become legally reviewable in any state court. Documentation of vetting — safety scores, inspection history, carrier agreements — becomes your first line of defense in a lawsuit, not just a compliance checkbox.

So what for brokers? The decision doesn't come until June, but the prep work starts now. Pull your carrier vetting SOP and ask: if you had to defend a specific carrier selection in court, could you? Document the criteria you use to approve carriers. If you're working with carriers that have never had a federal safety inspection — which, per the data, is most of them — make sure your contract language and vetting records are airtight. A ruling against the industry won't grandfather in your existing habits.

Brokers who've been winning on price by cutting corners on vetting have the most to lose. Brokers who've built carrier relationships on actual safety data have the least.

The ruling lands by June 30. That's 64 days.”

Meet Me For Coffee with Samantha Jones seeks to correlate macro-economics to freight markets (just like this Newsletter does) and offers a chance to hear various industry and non-industry experts explain their thoughts on economics and freight markets.

Check out our Podcast Channels on your preferred platforms!

If you attend no other supply chain conference all year, you must at least attend Manifest Vegas . I have been partnered with Manifest for the last 3 years and I cannot encourage you strongly enough to ATTEND THIS CONFERENCE. There is truly something for everyone. Yes, I know February 2027 is still a long ways off, but it comes up quick! And, if you know you have to attend, you might as well take advantage of early bird rates while you still can! Get the cheapest tickets possible now, and an ADDITIONAL $200 off with my unique link! Details and discount here: http://manifestvegas.com/MeetMeForCoffee

Thank you so much for reading and supporting the Truckload Market Update Report, produced by Samantha Jones Consulting LLC. Samantha Jones Consulting focuses on helping companies in the logistics industry better brand and sell their services to create sustainable revenue growth, and support their company growth goals!

We love Feedback, if you have questions, comments, suggestions, or are interested in sponsorships or partnerships, please email samantha@connectsjc.com to connect!

Make sure you subscribe to the Newsletter to receive the monthly update, and please share this with a friend who can also benefit from reading! As always, Samantha's work is free and created with the intent to add value to the transportation industry.