Happy Monday! We’ve almost made it through 2025. Looking back over the year, I have been covering many of the same topics each month. Is it repetitive? Yes. It is necessary? Also, yes. The focus of this report now for the last year has been on monitoring signs that there is a potential for change in the near future based on the current data and market trends we have available to us. As the longest freight downturn drags into 2026, we cannot quit caring about what happens when things begin to change. As always, those who are prepared will benefit the greatest.

So, what have we been monitoring this year that matters? Quite a few things, like labor markets, inflation, wage growth, consumer spending, consumer confidence and health, manufacturing PMI, current events, and truckload rates.

So let’s jump into some of those today, starting with current events.

As of last night, the Senate moved toward ending the longest government shutdown in US history. Eight democrats broke away from their party votes to join with Republicans in creating the 60-40 vote needed to start the beginning of the end for a government shutdown. They voted to pass a spending agreement that will fund the government through January, and provide affected federal workers with back pay, and reverse federal layoffs due to the shutdown. The bill will still need to formally pass the Senate and then approved by the House and signed into law by President Trump. So this won’t likely happen overnight, but progress is underway.

This definitely matters, because as long as the government has been shut down, economists and writers such as myself have had limited economic data sets to evaluate. We will have to wait until the government reopens and backlogged data is published to get the most up to date information for many statistics we monitor regularly to gauge the health and trajectory of the US economy. However, we are not completely blind, and some educational surveys and other data points have been released this month we will evaluate.

Two more current events before we move into economics. Trump finished his Asia tour, and many business deals were announced between the US and Asian countries Trump visited. Among those announcements was a 1 year “truce” of sorts between China and the US when it comes to retaliatory tariffs and fees. Again, nothing permanent, but a date out in the future in which things could again change. For the time being, the announcement seems to have given enough clarity to some importers to make some moves to import, with minor import bumps being noted on the China-west coast routes. Remember, most US Q4 imports were already brought into the country this summer.

The Supreme Court is currently hearing arguments on the IEEPA case. Matthew Leffler calls this the most important case in his lifetime, and it does have profound implications for supply chain but also for the US in general. This is the first time we have ever heard a case that will determine what exactly the extent of a President’s emergency orders can be. If nothing changes, we will set the precedent that a President can choose what is an emergency and what is not, and if tariffs are reversed to some extent, we will set the precedent that the Supreme Court ultimately decides what is emergent and what is not.

When it comes to tariffs, uncertainty still abounds, now with another looming date to keep it pushed out. We do not expect a final decision from the Supreme Court until early 2026. Some say maybe January, others say it could be later. At either rate, no supply chain decision makers will want to make major decisions now with a near future announcement on tariff policy looming. Things will remain on pause until the new year, another drag on business and economic activity.

Curious what the outcome of this case will be? We should be. Matthew Leffler has openly shared his predictions already, saying:

“Is it too early to call? After listening to over 2.5 hours of oral arguments, I don't think so. I predict a 6-3 or 5-4 ruling against the Trump administration by late spring 2026, invalidating the IEEPA-based tariffs as an unconstitutional overreach… This would affirm Congress's Article I primacy on taxation & commerce, trigger refunds for $88–$151 billion collected to date (potentially up to $750B+ with interest), & force Trump to pivot to alternative statutory tools like Section 232 or 301 of the Trade Act.”

Part of his confidence in this statement can be based on the comment made by Supreme Court Justice Gorsuch (a Trump nominated Justice):

"So congress as a practical matter, can't get this power back once it's handed it over to the president.. one way ratchet toward the gradual but continual accretion of power in the executive branch and away from the people's elected representatives."

So where do tariffs stand now and where would they stand if IEEPA reverses tariffs? Jan J. J. Groen had a great recent write up of this. Jan notes that as of today, we still have not seen the full inflationary impact of tariffs as they are trickling into the supply chain. So they are projected to still increase in effect until hitting an average effective rate of 17%. Jan says,

“The average effective tariff rate in the U.S., while already historically elevated, still does not reflect the full extent of the announced tariff hikes (chart above). According to the Yale Budget Lab, after readjusting some proclaimed tariff hikes that have not been implemented yet and clarifying USMCA exemptions, eventually (after consumption shifts of households and firms) the average effective rate will settle down at 17%. With the September average effective tariff estimated to have been at around 10.4%, there’s still a fair amount of tariff-induced price increases in the pipeline over the remainder of the year and going into 2026.”

He went on to address the impacts of an IEEPA case decision that would overturn the tariff announcements. A reversal won’t remove ALL tariff updates, but many of them.

“One downside risk to this aspect of the inflation outlook, is the potential dismissal by the Supreme Court of the tariff hikes implemented under the IEEPA. If SCOTUS indeed dismisses these hikes in June 2026, the long-term average tariff rate will drop from currently 17% to 6.8% (orange vs green bar in the above chart), as such a ruling would wipe out about 71% of the announced tariff hikes.”

Here is the referenced chart:

So tariffs may be reversed, they may not be, but either way there will still be some tariff increases allowed to remain. And, we won’t know for sure until sometime in spring of 2026, with reversal efforts taking even longer. And if they are reversed, the Trump administration has already said they would seek alternate ways to keep tariffs in place. AND, as a last note, Trump announced via Truth Social that they are looking to provide a tariff rebate of sorts to the American people in the form of up to $2,000 credits come tax time. Minimal details on this as of now, but this is not the first time this idea has been floated. Personal financial stimulus always has the potential to create a consumption stimulus, and investors are already tracking this headline.

A huge thank you to BiggerPicture for sponsoring this month's newsletter! BiggerPicture is focused on helping shippers, brokers, and carriers maximize their operational productivity, by reducing the time spent scheduling appointments by an average of 80%. Achieve full ROI in 3 months or less, and unlock new growth potential by shifting your most valuable resources (your peoples' time) where it can make the biggest impact.

Moving on, news into economics now. The FED announced another .25 bps rate cut. This triggered the average mortgage rate in the US to decline slightly to 6.71%, the lowest it has been in a year. Still too high to convince homeowners with a 2-3% interest rate to move. I was just speaking with my neighbors who built and closed on their home about a year before I did, and they are on a 2.25% interest rate. They are not interested in moving anytime soon to say the least. This still elevated mortgage rate, combined with high home prices and many feeling locked into low mortgage rates has kept the residential housing market suppressed. This is unfortunate for freight, as the residential housing market alone can be a great demand side stimulus in strong market conditions (like 2020-2021).

But herein lies the problem with FED rate cuts. The more they cut while inflation is still showing persistence, the more they risk losing their credibility that they are able to stick to a 2% inflation rate. Because, inflation is not at 2%, it’s at ~3% still. Policy easing could then be said to be due to labor market weakness, but the health of the labor market is being actively debated from what I read each month. There are those who argue it is better off than it appears, and those who argue it is worse off than it appears.

Here is what we SHOULD NOT do right now. Confuse consumer sentiment with actual consumer health. Consumer confidence reports have been loud. Would you be shocked if I told you that the reality is that most Americans are financially healthy right now?

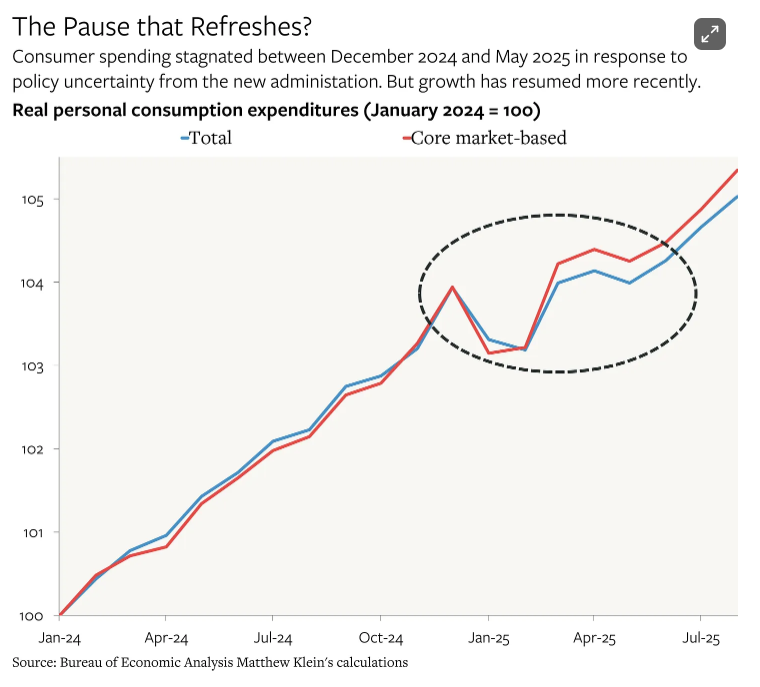

I frequently cite Matthew Klein in my work, and the reason for that is because his work has great depth to it. I don’t have to go pull you 7 articles citing different studies and data points, because he has written one article that does all of that. In his recent publication, he makes a case for the strength of the American consumer.

As I was preparing to have to contrast his stance to the recent negative headlines regarding consumer sentiment (see here and here), I got to the part of his article where he already did that.

We have been hearing a lot about consumer pullback because of inflation and financial stress. I have been covering the strong position of Americans because of wage growth outpacing inflation, and a higher than pre-pandemic personal savings rate. Matthew went a step farther to include the wealth many Americans are generating from assets right now in a strong market environment, and in the strong positions many households have by not owning their goods on credit. Now more than ever in recent years, American households have purchased durable goods with cash over credit. So we find ourselves in a position where households have either necessary durable goods paid off and on hand, savings put up, assets providing returns, or some combination of more than one of these factors.

Consumer sentiment has been detaching itself further from consumer behavior now for years, so the recent results don’t surprise me much. And I don’t think we can give them too much weight. Especially when it seems that (at least before we lost visibility into data because of the government shutdown) spending was on the rise again after some initial pause and caution used due to tariff announcements and inflationary fears.

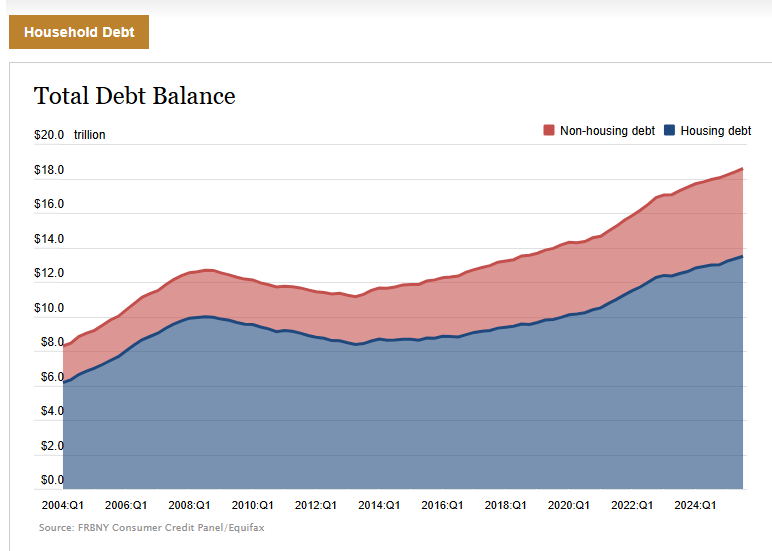

Household Debt

US Households have taken on more debt this year, we can see that, it also is interesting to see it track mortgage activity. When people move, they spend. Many spend on credit. Debt is up about 1% nationally from last year at this time. We can keep an eye on this, but we also have to evaluate it alongside the other measures I have continued to review, like personal savings rates, wage growth, and consumer spending.

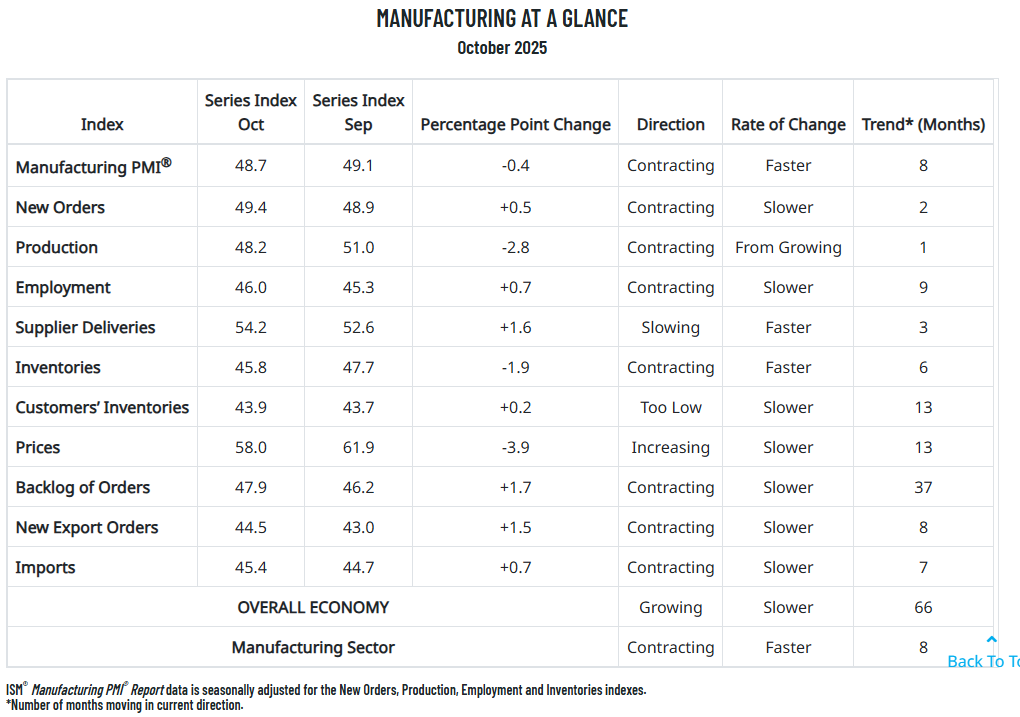

Manufacturing

Overall, manufacturing is still in contraction. Readings below 50 in particular are considered contractionary. Overall Manufacturing PMI in October was 48.7, down from 49.1 in September. Backlog of orders is an important data point to watch because a growing backlog would require growing material inputs and order outputs. We should particularly be watching this because Customers’ Inventories have been running “too low” for months, and will be more sensitive to demand changes.

Rather than write up a summary of this section before moving onto truckload rates, I thought I’d share another great source. I am a monthly reader of the Arrive Logistics market report, and I read the most recent publication after drafting the outline for my report this month. I was pleased to see how similarly aligned we were this month. So, I will offer up to you their summation of the current environment:

“Consumers are still spending amid labor market challenges, but inflation and higher borrowing costs will continue to weigh on durable goods demand, and limited visibility into tariff timing and scope adds uncertainty to the volume outlook. With most holiday freight already pulled forward earlier in the year, a muted peak season appears likely. While supply is solid for now, low equipment orders and long-term regulatory impacts will make capacity increasingly vulnerable to demand shocks. Consumer spending held steady in September, and while the latest CPI reading has yet to be released, it’s expected to remain within recent ranges. With that, and without new labor data available at the time of writing, the broader economic picture remains largely unchanged from last month. Looking Ahead - Economic conditions should help keep freight volumes at or near current levels. However, interest rates, inflation and labor uncertainty remain risks. Further rate cuts would help stimulate housing and durable goods demand, which in turn would greatly benefit freight volumes.”

Before I move on, because this is already pretty lengthy, I wanted to link a source for anyone who is curious to keep up with AI. AI is essentially single handedly propping up the US stock market at this time, and business spending and investment in the US is largely due to AI. So, I think it’s worth staying educated on. This article is an interesting angle, and details how even all the tariff policy is still leaving carveouts to help drive investment towards data centers and the infrastructure that is critical for AI to succeed.

“the Trump administration is increasingly gambling the future of the American economy on AI. If they’re right, the US will capture the dual rewards of both coding the tools of the next economic revolution and owning the infrastructure that runs it. If they’re wrong, the US will be left with a bunch of distressed assets and will have dramatically underinvested in the projects that actually mattered. The large tariff exemption for computers is distorting the American economy in ways that could reshape the long-run future of the country. Yet in the short run, it’s undeniable that the carveout has achieved its desired effect of accelerating America’s AI boom. The US is at the technological forefront of a rapidly expanding industry because of the free trade policies that this administration ostensibly despises. It’s just tragic that this privilege is not extended to businesses outside Silicon Valley.”

To start, let's talk about supply. Our economics section focuses on factors that impact demand. Factors that impact carrier capacity (supply) are also important to track.

In October, according to FMCSA data, we saw 4800 carriers leave and 5,000 new carriers enter, a net increase of 132 carriers. This is the closest we have been to neutral since March. As long as we remain close to neutral, we are in a stable environment because demand has been so stable, not rising or falling. We could take a couple of things from this. One is that we still have a constant flow of new entrants. Despite the concern of carriers exiting due to things like ELP and Non-Domiciled CDLs, we still see a stream of new entrants. Did you know that every year, an average of 450,000 CDLs are issued? We are a high churn industry, and capacity seems to always flow in to replace exits.

The debate around the ability of non-domiciled CDL holders to have a significant enough impact on supply to create market imbalance in 2026 is ongoing. This Thursday, November 13th, I have heard that Ken Adamo from DAT plans to debate this topic with Craig Fuller from Freightwaves, moderating the conversation is Matthew Leffler. Perhaps both view points regarding this topic will be represented.

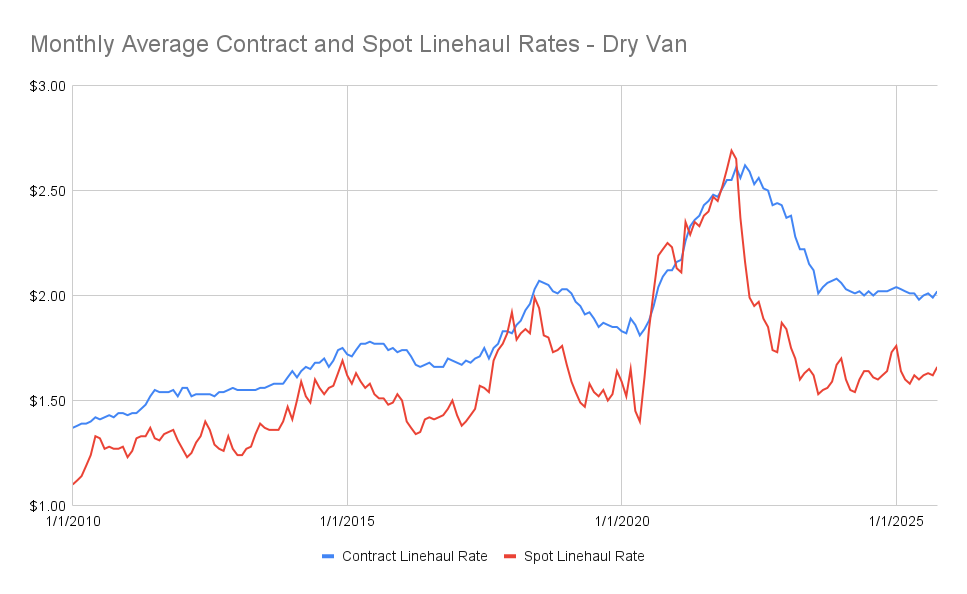

Next, it’s worth noting that diesel prices are up .22 YOY. Rates have not changed much, and so fuel prices increasing is never a welcome pressure. There has been some volatility in fuel prices recently, but we can probably expect some stabilization soon as crude prices stabilize and diesel prices settle.

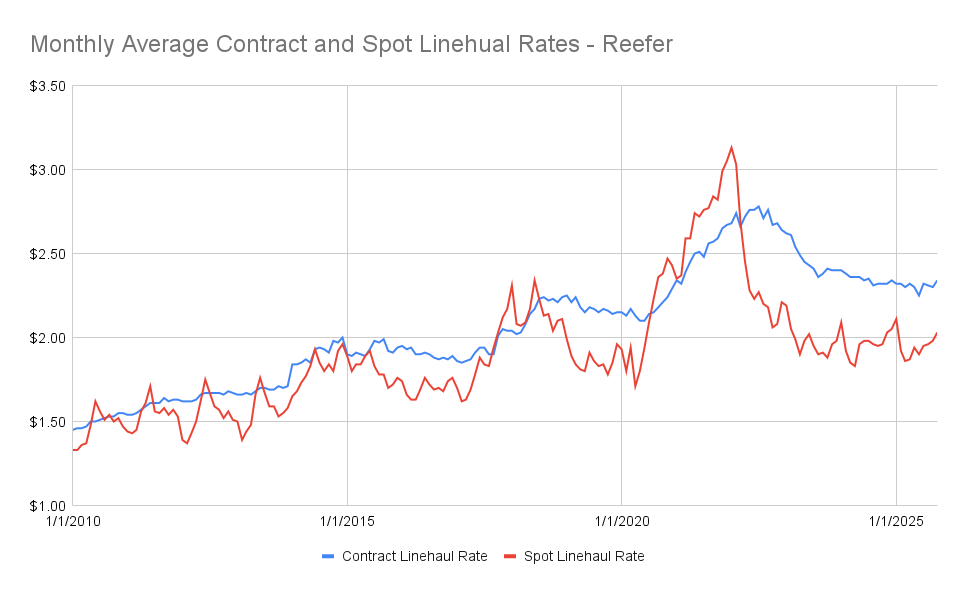

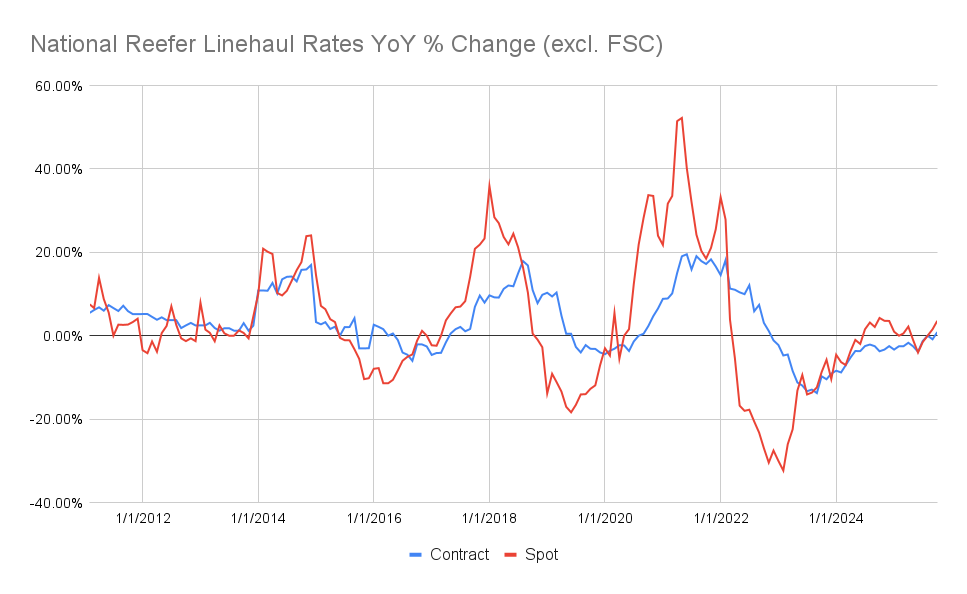

October spot rates did not keep their early October momentum. In the last report I said it will remain to be seen if we could keep building momentum, and we did not at the pace set in early October. In fact the last couple of weeks saw rates decrease across all modes. There have been some modest gains in pricing overall the last couple of months, but when you look at the gap between spot and contract we still see plenty of white space. Reefer rates will likely see some traction leading up and through the holidays as well, so keep that in mind as November kicks of the Holiday season!

Meet Me For Coffee with Samantha Jones seeks to correlate macro-economics to freight markets (just like this Newsletter does) and offers a chance to hear various industry and non-industry experts explain their thoughts on economics and freight markets.

Thank you to our sponsor, Watco Logistics. As a leading 3PL, Watco Logistics provides rail, highway, intermodal, e-commerce and fulfillment, barge, international and cross-border solutions. At the core, Watco Logistics specializes in solving unique supply chain challenges. Learn more about Watco Logistics here!

Check out our Podcast Channels on your preferred platforms!

Save Money On Conferences!

Here is where Samantha is heading next, take advantage of her media sponsorship with these conferences to save $$ on your own registration! Questions about these shows, not sure which ones are for you? Message Samantha!

Discount to save $200 on your Manifest: The Future of Supply Chain & Logistics registration! ManifestVegas.com/MeetMeForCoffee

Thank you so much for reading and supporting the Truckload Market Update Report, produced by Samantha Jones Consulting LLC. Samantha Jones Consulting focuses on helping companies in the logistics industry better brand and sell their services to create sustainable revenue growth, and support their company growth goals!

We love Feedback, if you have questions, comments, suggestions, or are interested in sponsorships or partnerships, please email samantha@connectsjc.com to connect!

Make sure you subscribe to the Newsletter to receive the monthly update, and please share this with a friend who can also benefit from reading! As always, Samantha's work is free and created with the intent to add value to the transportation industry.