A September Fed rate cut? The Federal Open Market Committee (FOMC) meets September 16-17th to decide on the current state of monetary policy and any interest rate cuts. Last month the Fed chose to hold rates but I started to build the case that the revised labor market data could be reason enough for them to consider cutting rates at the next meeting. Now, most gauges for probability have a September rate cut at a 90-100% likelihood. As we have discussed plenty in previous reports, the Fed has two main priorities: control inflation, and keep a healthy labor market. Economists are anticipating a rate cut this September, however, I’d caution it might not be the start of aggressive cutting for the remainder of the year. A cut in September because the labor market is becoming questionable, and at the same time a still conservative stance throughout Q4 because inflation remains questionable.

Let’s quickly unpack.

Fortune published an article quoting Moody’s Analytics chief economist Mark Zandi saying,

This really feels like a jobs recession. Employment is flat to down. Output and incomes are still growing, but the economy is incredibly vulnerable. Nothing else can go wrong, or it could tip us into a full downturn.”

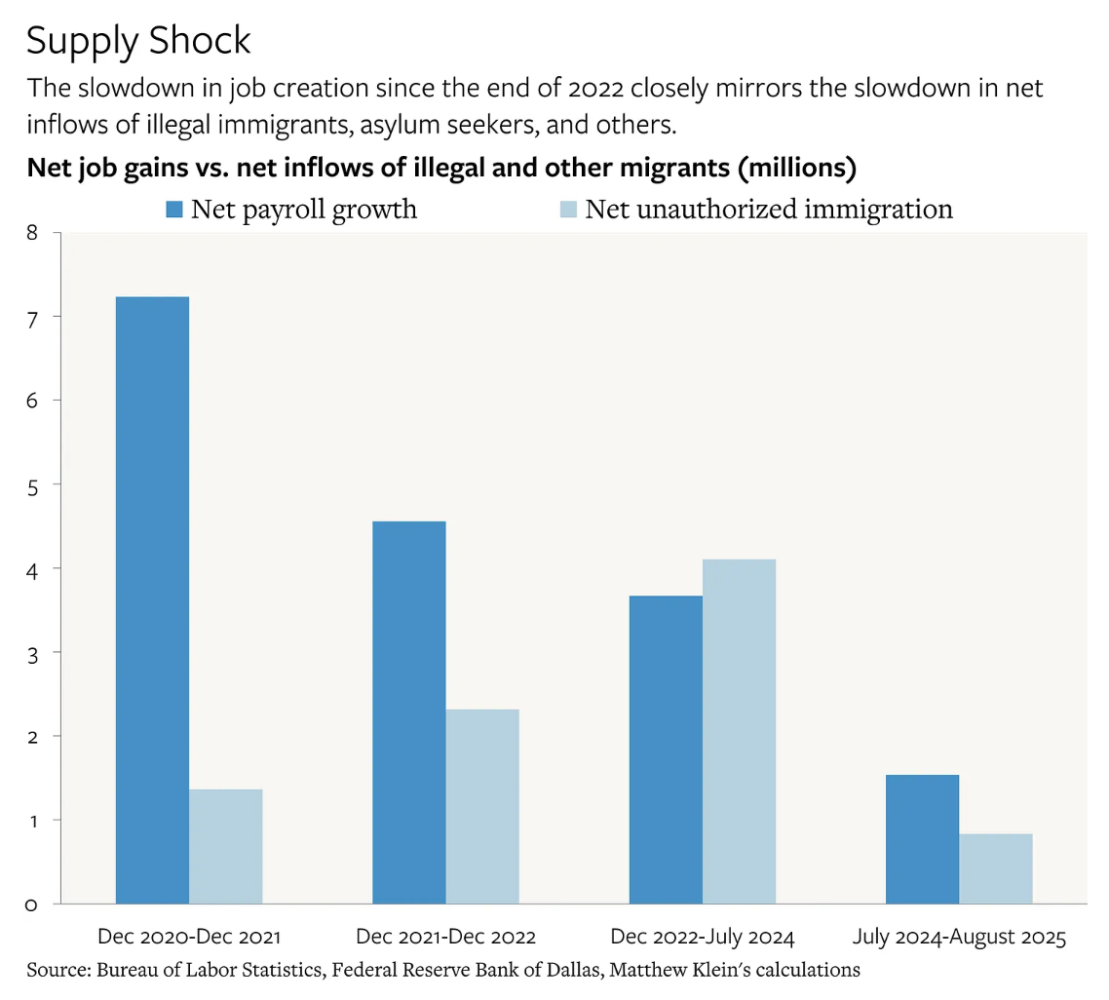

That’s a really critical way of putting it, especially considering a popular measure of a recession is negative GDP and we are on track for 3% GDP growth in the 3rd quarter. However, some negativity is warranted. All job gains were in healthcare or hospitality related fields. Aside from these minimal freight generating sectors, employment is down and new job growth is down. Scott Bessent responded directly to Zandi’s commentary by saying August is always the noisiest month of the year, with big revisions later to come most likely. He also said if these numbers are true, the Federal Reserve should have cut rates sooner, knowing the bad data was going to be lagging.

Jan J. J. Groen wrote a very thorough article last week breaking down the recent data release. The trouble with the jobs data is it’s forcing the Fed to work harder to balance their two goals. While hiring is slowing and unemployment is ticking up ever so slightly, wage growth is still occurring and adding to inflation pressures. He believes there is enough labor market uncertainty right now to justify a small September cut, but anything beyond that is unlikely for the rest of the year.

“Given the imminent possibility of a 25bps rate cut in September I’ll change my Fed call for 2025 from no rate cuts to one. Inflation stickiness, solid consumption spending and gradual easing in the unemployment rate will deter most FOMC member from pursuing multiple rate cuts beyond September.”

Matt and JJ were almost entirely in line with their commentary this month, with Matthew Klein writing,

Instead, the latest numbers on jobs and incomes are consistent with the view I have had for some time: real growth has been relatively stable after accounting for changes in net immigration, while nominal growth remains persistently faster than would be consistent with 2% inflation. This suggests that it would be unwise for the Federal Reserve to unleash the latent financial firepower of consumers and businesses by lowering borrowing costs much further from current levels, if at all.

Lastly, I wanted to see what Gad Levanon had to say about the labor market data. He joined me on my podcast recently, and labor markets are really his area of expertise, and we discussed how AI and productivity enhancements will continue to impact the US economy. Gad also acknowledged the effects of immigration on the labor market in his latest publication, and then on productivity he said this,

3) Productivity and automation. We are in a period of high labor productivity growth. Firms learned to run lean during the 2021–23 labor squeeze and have kept upgrading processes—better logistics, workflow automation, and now AI-assisted tools. Higher output per hour reduces the need to add headcount for a given level of demand; some firms are also trimming roles in anticipation of near-term AI gains.

And he even included a 12 month forward-looking prediction:

"The next 12 months: a baseline GDP: ~2% growth. Jobs: positive but low, averaging ~50k per month. Unemployment: essentially flat or a slow drift higher. Demand should remain decent—helped by the AI-infrastructure buildout—but consumption is the swing factor if slower job and population growth bite. Immigration will remain restrictive relative to 2021–23, however, the marginal impact from undocumented workers opting out due to deportation fears may begin to plateau. Productivity could push higher as more firms deploy AI-based automation. Recession check - The NBER calls recessions “a significant decline in economic activity that is spread across the economy and lasts more than a few months.” That’s not today’s picture with GDP running above trend. However unlikely, even a brief period of slightly negative payroll prints alongside solidly expanding GDP would not meet the NBER standard—but it would definitely intensify the debate.”

How Do Brokers Protect Profits in 2025? Rates are tight, costs are climbing but with Tai TMS, smart brokers are finding ways to grow. This eBook breaks down how top brokers use better carrier management, real-time data, and automation to protect margins in a tough market. Read Here

MarketWatch covered some commentary made by the New York Fed President John Williams, they wrote:

“Williams’ forecast on inflation was more benign. He said inflation will spike above 3% in the near term before trending down to 2.5% in 2026 and 2% in 2027.” and that “he has not seen evidence that higher White House tariffs on imported goods have caused a spike in general inflation trends.”

Of course, it seems that the Fed is prepping their explanation for the September rate cut that is highly expected to occur. The St Louis Fed President said he sees inflation spiking in the near term, but easing back to the 2% target in 2026.

Inflation data should release sometime this week, but here are the latest Cleveland Fed predictions for inflation:

Edward Jones also is calling for near term inflation to bump up slightly, but highlights opportunities for core CPI to decrease in the coming months as well.

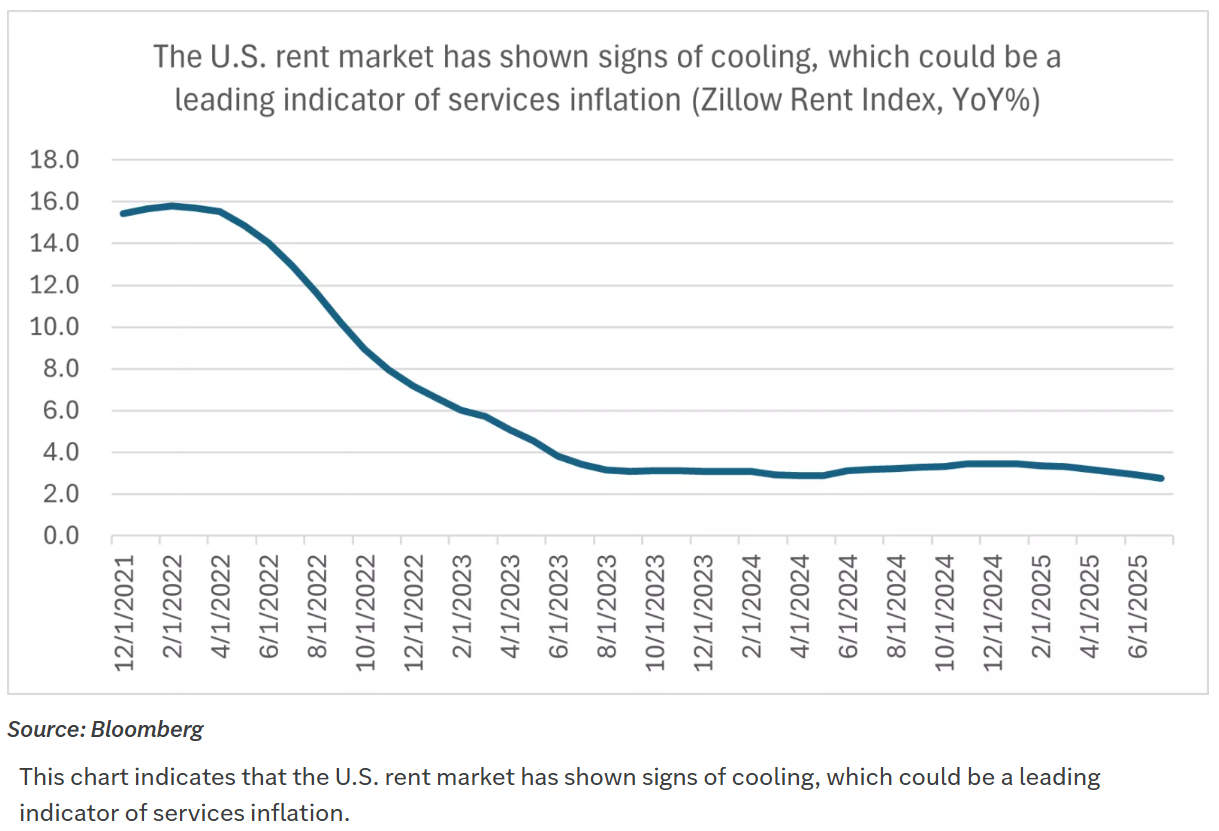

“The expectation is that headline CPI inflation will tick higher to 2.9% annually, up from 2.7% last month, although core CPI, excluding food and energy, will remain steady at 3.1%1. PPI inflation is forecast to tick lower from 3.7% to 3.5%, while core PPI is expected to fall from 3.3% to 3.2%1. Both sets of inflation metrics remain above the Fed's 2% target, and the higher PPI inflation implies that companies are still facing pricing pressures from their wholesalers, likely driven in part by higher tariff rates. Nonetheless, we think there are a couple of mitigating factors to the inflation rates that continue to remain above target and are in some cases creeping higher. First, as the Fed has indicated, tariff-induced inflation on goods may continue to show up in the months ahead, but we would also expect inflation rates to stabilize and move lower after the one-time step-ups in prices are realized. And second, while goods inflation makes up about 33% of the inflation basket, services inflation makes up about 66%. If services inflation, which include shelter and rent pricing, start to soften, especially as the labor market softens, we could still see overall inflation rates remain steady or even move lower.”

I really took some time on the labor data above because it helps better explain inflation and manufacturing. Factory jobs and jobs across manufacturing have seen negative growth over the last four months. Understandably, skeptics are wondering where all the jobs are going to come from that the current administration has promised to American workers. On the same interview I referenced previously, Scott Bessent said, “It’s been a couple of months, and with the manufacturing sector as you know, we can’t snap our fingers and have factories built”. He went on to say the OBBBA being passed in July helped to unleash investment hesitations for businesses operating and investing in America. Time will tell if additional investments will come in US manufacturing.

For now, the August Manufacturing PMI data had a small increase from July of .7%, but new orders were up to 51.4 from 47.1. We will have to see if Q4 brings with it opportunities for manufacturing activity to begin expanding. Consumer surveys are slowly growing in optimism but they still expect near term inflation to be a factor, and we have seen consumers becoming more cautious with goods’ spending.

A huge thank you to BiggerPicture for sponsoring this month's newsletter! BiggerPicture is focused on helping shippers, brokers, and carriers maximize their operational productivity, by reducing the time spent scheduling appointments by an average of 80%. Achieve full ROI in 3 months or less, and unlock new growth potential by shifting your most valuable resources (your peoples' time) where it can make the biggest impact.

I’ve now been authoring this newsletter for over three years, and one theme has become increasingly clear: economics and politics are converging. What I mean by this is that the economy is no longer shaped primarily by domestic factors alone, it is being heavily influenced by global geopolitical events. The pandemic was the first major shock, followed by rolling recessions in different parts of the world, the war in Ukraine, conflict in Gaza, and shifting U.S. trade policies where tariffs are driven as much by geopolitics as by economics.

Why does this matter? Because these overlapping forces have made predicting the economy more complex than it was pre-pandemic. Freight professionals know this firsthand. We are navigating one of the longest and deepest freight down cycles, yet consumer spending and load volumes have remained relatively healthy through much of it. It’s a reminder that the old models don’t always apply, and that the dynamics shaping markets are evolving.

To keep perspective, I’ve found it useful to follow a range of economists with different approaches. For example, Matthew Klein often calls things as he sees them, sometimes more optimistic than consensus, other times more pessimistic. By balancing views that are negative, middle-ground, and optimistic, I try to represent a fuller picture in my own writing. I encourage you to do the same, and I hope this newsletter serves as one of those resources.

As we head into Q4 and prepare for a new year, it’s more important than ever to understand how economics and monetary policy intersect with business decisions. Doing so helps you better anticipate where your customers and partners stand, what risks they’re weighing, what investments they’re making, and what precautions they’re taking.

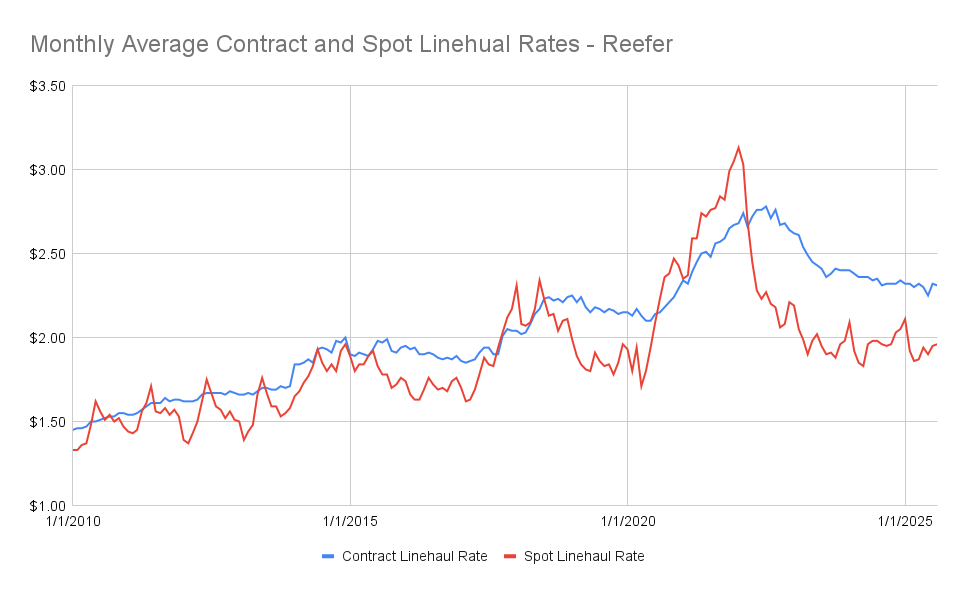

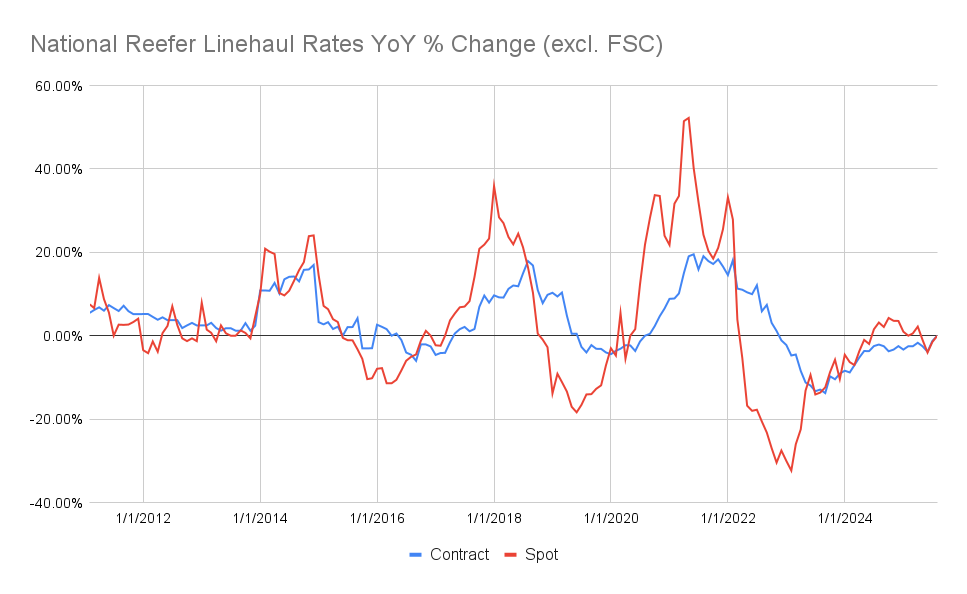

For now, truckload rates remain largely unchanged. And I’m struggling to see a demand side catalyst in Q4 of this year, so I would expect rates to remain comparable to Q4 of last year. The English Language Proficiency mandate had some people hopeful it would remove enough capacity to strain the market into tightening, but so far we are not seeing that supported in the data. Perhaps it will take longer for the full effects to kick in, but right now, if it has impacted capacity, it appears there was plenty more to step in and take its place.

Here’s a look at the charts DAT provides each month on updated reefer and dry van spot and contract rates.

Meet Me For Coffee with Samantha Jones seeks to correlate macro-economics to freight markets (just like this Newsletter does) and offers a chance to hear various industry and non-industry experts explain their thoughts on economics and freight markets.

Thank you to our sponsor, Watco Logistics. As a leading 3PL, Watco Logistics provides rail, highway, intermodal, e-commerce and fulfillment, barge, international and cross-border solutions. At the core, Watco Logistics specializes in solving unique supply chain challenges. Learn more about Watco Logistics here!

Check out our Podcast Channels on your preferred platforms!

Save Money On Conferences!

Here is where Samantha is heading next, take advantage of her media sponsorship with these conferences to save $$ on your own registration! Questions about these shows, not sure which ones are for you? Message Samantha!

The JOC Inland Distribution Conference is coming up soon in September! I have a code to save you 15% off your registration! COFFEEINLAND25 https://inland.joc.com/en/register Want to know if Inland is for you? Check out this video!

Discount to save $200 on your Manifest: The Future of Supply Chain & Logistics registration! ManifestVegas.com/MeetMeForCoffee

Thank you so much for reading and supporting the Truckload Market Update Report, produced by Samantha Jones Consulting LLC. Samantha Jones Consulting focuses on helping companies in the logistics industry better brand and sell their services to create sustainable revenue growth, and support their company growth goals!

We love Feedback, if you have questions, comments, suggestions, or are interested in sponsorships or partnerships, please email samantha@connectsjc.com to connect!

Make sure you subscribe to the Newsletter to receive the monthly update, and please share this with a friend who can also benefit from reading! As always, Samantha's work is free and created with the intent to add value to the transportation industry.